- +1-315-215-1633

- sales@thebrainyinsights.com

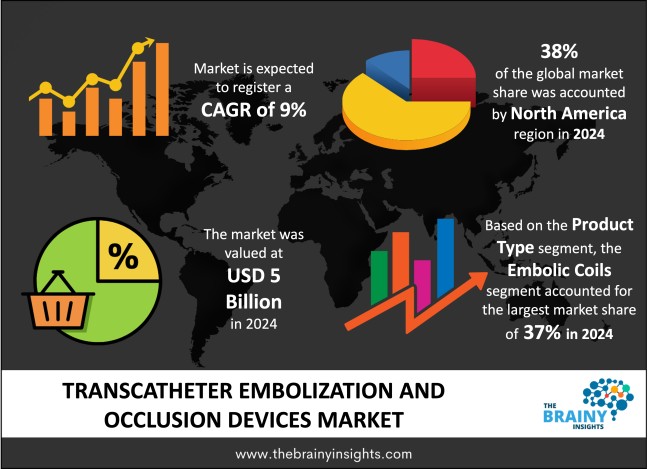

The global transcatheter embolization and occlusion devices market was valued at USD 5 billion in 2024 and grew at a CAGR of 9% from 2025 to 2034. The market is expected to reach USD 11.83 billion by 2034. The increasing healthcare expenditure will drive the growth of the global transcatheter embolization and occlusion devices market.

Medical treatments require the use of minimally invasive transcatheter embolization and occlusion devices for blood vessel flow restriction or blockage purposes. These medical devices form essential elements of medical treatments because they are used for aneurysm, AVM patients and those with tumours and gastrointestinal bleeding issues. The medical personnel use fluoroscopic imagery to guide a catheter from an incision in the groin or wrist to reach the blood vessel target. The medical interventionalist places the delivery system into its targeted position before introducing embolic agents consisting of coils, plugs, liquid embolic, or microspheres for blocking the vessel either temporarily or permanently. The selection of embolic material depends on how big the vessel is and its flow characteristics and what final result doctors want to achieve. The medical devices find extensive applications across interventional radiology, cardiology and neurology. Patients who cannot have open surgery benefit from transcatheter embolization as an alternative since this method requires shorter recovery times and minimizes surgical difficulties and results in low postoperative risks as well as reduced procedural intervention. These markets continue growing because of rising geriatric populations and better healthcare system development in emerging countries. Furthermore, TEO devices will experience sustained innovation because future developments will focus on bioresorbable embolic materials alongside advanced imaging techniques and AI-driven navigation systems which will improve precision and patient outcomes.

Get an overview of this study by requesting a free sample

The increasing incidence and prevalence of chronic diseases – Patients require transcatheter embolization and occlusion devices due to the increased number of cardiovascular, neurological conditions and cancer cases. The aging population also contributes to this market’s growth. Cardiovascular diseases (CVDs) consisting of aneurysms and arteriovenous malformations (AVMs) and strokes remain the principal factors that cause mortality and morbidity. Treatments that use transcatheter embolization are effective and are preferred to treat the increasing prevalence of blood vessel disorders. Transcatheter embolization serves as a minimally invasive approach to treating cerebral aneurysms since it replaces the need for open surgical procedures. The market experiences growth because of increasing global cancer incidents that demand embolization procedures as essential tumour management tools for liver, kidney and prostate cancer treatment. Transcatheter treatments have successfully developed as valuable therapeutic alternatives because they produce better outcomes for patients with fewer systemic side effects. TEO devices face growing market demand because the aging global population consists of individuals whose bloodstream is more prone to develop vascular problems which include aneurysms and tumours. Traditional surgical procedures become too risky for aging patients because of their medical conditions which makes the minimally invasive embolization technique more appealing. The growing elderly population together with lengthening lifespan in developed economies will bolster the demand for embolization procedures.

High costs of transcatheter embolization and occlusion devices – The production of embolic agents including drug-eluting microspheres, bioresorbable materials and liquid embolic requires sophisticated manufacturing technology because they must meet advanced biocompatibility standards that increases their manufacturing expenses. The complete set of microcatheters alongside imaging systems and navigation tools causes financial difficulties during embolization treatments which impact both healthcare institutions and patients. Costs escalate due to the requirement of premium imaging technologies. The expense of embolization procedures increases because of the specialized knowledge which makes them possible. Proficiency in interventional radiology requires doctors and physicians to complete extensive training programs because their specialist skills have premium pricing. Embolization procedures remain scarce throughout developing nations because there is a shortage of expert medical staff which leads procedures to concentrate mainly in high-end medical facilities. The payment rules presented discrepancies among different healthcare systems because they often limit the coverage for embolization procedures. Patients in nations with insufficient insurance coverage have to pay medical expenses from their pocket funds thus reducing healthcare accessibility. This reduces the spread of TEO devices in spite of their established medical advantages.

Increasing research and development expenditure – The TEO device market demonstrates strong expansion because of new technologies in embolic materials and catheters and expanding healthcare facilities across emerging markets. Embolic material innovations continue to enhance both procedural safety characteristics as well as procedural efficiency. Current advances in catheter technologies with improved flexibility have produced more navigable microcatheters along with imaging systems that facilitate safer and more accessible embolization procedures for intricate vascular structures. Delayed healthcare infrastructure growth in emerging markets accompanies quick infrastructure development to offer greater accessibility to advanced interventional procedures. Governments throughout Asia-Pacific along with Latin America and Middle Eastern territories invest into modern medical facilities and enhanced reimbursement systems to foster medical travel programs that enhance the adoption of TEO devices. Healthcare providers along with patients who become better informed about embolization procedures enhance the market demand in emerging areas.

The regions analysed for the market include North America, Europe, South America, Asia Pacific, the Middle East, and Africa. North America emerged as the most significant global transcatheter embolization and occlusion devices market, with a 38% market revenue share in 2024.

The region maintains first-class healthcare infrastructure alongside high disease prevalence rates along with strong presence of key market players. North America holds the leading position in medical device markets because of its high numbers of patients needing embolization treatment for cerebral aneurysms and arteriovenous malformations. The increasing number of elderly people who face higher susceptibility to vascular diseases and tumour-related conditions also require embolization treatments. The positive reimbursement policy for embolization procedures in the region increase healthcare accessibility. Medical device producers Medtronic, Stryker, and Boston Scientific operate within North America and invest continuously in developing innovative embolization technologies through their research-and-development efforts. The market grows because of the skilled interventional radiologists working in the field and rising public understanding about minimally invasive techniques. The global TEO devices market will continue to have North America in the leading position based on these established factors.

North America Region Transcatheter Embolization and Occlusion Devices Market Share in 2024 - 38%

www.thebrainyinsights.com

Check the geographical analysis of this market by requesting a free sample

The product type segment is divided into embolic coils, liquid embolic agents, embolic plug systems, detachable balloons, and flow diverters. The embolic coils segment dominated the market, with a market share of around 37% in 2024. Both clinical success rates and market dominance of TEO devices belong to embolic coils because they excel in treating various vascular malformations. The precision together with reliability and different anatomical structure compatibility makes embolic coils the most preferred option for interventional radiologists and neurosurgeons. The wide utilization of embolic coils in neurovascular procedures where they treat intracranial aneurysms represents a major reason for their prevalence. The technology of coils has evolved through newer flexible and soft designs that boost both their transport feasibility and density for packing which leads to better treatment results. Embolic coils have become more widely useful because they adapt to microcatheter systems and medical applications across different specialties. Greater patient choice of minimally invasive treatments and ongoing coil material research and deployment method advancement positions embolic coils to remain the dominant segment in TEO devices market with sustained market demand and technological development throughout the coming years.

The application segment is divided into neurology, cardiology, oncology, urology and peripheral vascular diseases. The neurology segment dominated the market, with a market share of around 38% in 2024. Transcatheter embolization and occlusion devices market leadership stems from neurology applications because cerebral aneurysms together with arteriovenous malformations (AVMs) and ischemic strokes have high disease frequency. The precise nature of these medical conditions leads therapeutic teams to prefer embolization as the primary treatment method. The standard transcatheter embolization procedure currently uses embolic coils and liquid embolic agents to handle intracranial aneurysms which reduces healthcare risks from open surgical procedures like clipping. Token embolization techniques in neurology have gained increased demand because of the expanding number of worldwide stroke and haemorrhagic events. TEO devices market will continue to use neurology primarily due to persistent advancements in technology and increasing understanding of its benefits.

The end-user segment is divided into hospitals, ambulatory surgical centres (ASCs) and specialty clinics. The hospitals segment dominated the market, with a market share of around 61% in 2024. The primary healthcare facilities execute most embolization procedures to treat neurovascular, cardiovascular and oncological conditions because they specialize in handling complex medical needs. Hospital dominance as a healthcare facility stems from their extensive patient care capabilities throughout every diagnosis through to post-procedure observation. Hospitals enable embolization procedures by making high-end imaging technologies accessible for medical professionals. Hospital operating rooms with integrated catheterization labs deliver real-time medical imaging during specific embolization treatments which increases procedural performance results. Hospitals receive advantageous payment programs which create better patient access to embolization procedure services. High-cost embolization treatments in developed regions receive support from government and private healthcare funding so hospitals strengthen their position as market leaders.

| Attribute | Description |

|---|---|

| Market Size | Revenue (USD Billion) |

| Market size value in 2024 | USD 5 Billion |

| Market size value in 2034 | USD 11.83 Billion |

| CAGR (2025 to 2034) | 9% |

| Historical data | 2021-2023 |

| Base Year | 2024 |

| Forecast | 2025-2034 |

| Region | The regions analysed for the market are Asia Pacific, Europe, South America, North America, and Middle East and Africa. Furthermore, the regions are further analysed at the country level. |

| Segments | Product Type, Application and End User |

As per The Brainy Insights, the size of the global transcatheter embolization and occlusion devices market was valued at USD 5 billion in 2024 to USD 11.83 billion by 2034.

Global transcatheter embolization and occlusion devices market is growing at a CAGR of 9% during the forecast period 2025-2034.

The market's growth will be influenced by the increasing incidence and prevalence of chronic diseases.

High costs of transcatheter embolization and occlusion devices could hamper the market growth.

This study forecasts revenue at global, regional, and country levels from 2021 to 2034. The Brainy Insights has segmented the global transcatheter embolization and occlusion devices market based on below mentioned segments:

Global Transcatheter Embolization and Occlusion Devices Market by Product Type:

Global Transcatheter Embolization and Occlusion Devices Market by Application:

Global Transcatheter Embolization and Occlusion Devices Market by End-User:

Global Transcatheter Embolization and Occlusion Devices Market by Region:

Research has its special purpose to undertake marketing efficiently. In this competitive scenario, businesses need information across all industry verticals; the information about customer wants, market demand, competition, industry trends, distribution channels etc. This information needs to be updated regularly because businesses operate in a dynamic environment. Our organization, The Brainy Insights incorporates scientific and systematic research procedures in order to get proper market insights and industry analysis for overall business success. The analysis consists of studying the market from a miniscule level wherein we implement statistical tools which helps us in examining the data with accuracy and precision.

Our research reports feature both; quantitative and qualitative aspects for any market. Qualitative information for any market research process are fundamental because they reveal the customer needs and wants, usage and consumption for any product/service related to a specific industry. This in turn aids the marketers/investors in knowing certain perceptions of the customers. Qualitative research can enlighten about the different product concepts and designs along with unique service offering that in turn, helps define marketing problems and generate opportunities. On the other hand, quantitative research engages with the data collection process through interviews, e-mail interactions, surveys and pilot studies. Quantitative aspects for the market research are useful to validate the hypotheses generated during qualitative research method, explore empirical patterns in the data with the help of statistical tools, and finally make the market estimations.

The Brainy Insights offers comprehensive research and analysis, based on a wide assortment of factual insights gained through interviews with CXOs and global experts and secondary data from reliable sources. Our analysts and industry specialist assume vital roles in building up statistical tools and analysis models, which are used to analyse the data and arrive at accurate insights with exceedingly informative research discoveries. The data provided by our organization have proven precious to a diverse range of companies, facilitating them to address issues such as determining which products/services are the most appealing, whether or not customers use the product in the manner anticipated, the purchasing intentions of the market and many others.

Our research methodology encompasses an idyllic combination of primary and secondary initiatives. Key phases involved in this process are listed below:

The phase involves the gathering and collecting of market data and its related information with the help of different sources & research procedures.

The data procurement stage involves in data gathering and collecting through various data sources.

This stage involves in extensive research. These data sources includes:

Purchased Database: Purchased databases play a crucial role in estimating the market sizes irrespective of the domain. Our purchased database includes:

Primary Research: The Brainy Insights interacts with leading companies and experts of the concerned domain to develop the analyst team’s market understanding and expertise. It improves and substantiates every single data presented in the market reports. Primary research mainly involves in telephonic interviews, E-mail interactions and face-to-face interviews with the raw material providers, manufacturers/producers, distributors, & independent consultants. The interviews that we conduct provides valuable data on market size and industry growth trends prevailing in the market. Our organization also conducts surveys with the various industry experts in order to gain overall insights of the industry/market. For instance, in healthcare industry we conduct surveys with the pharmacists, doctors, surgeons and nurses in order to gain insights and key information of a medical product/device/equipment which the customers are going to usage. Surveys are conducted in the form of questionnaire designed by our own analyst team. Surveys plays an important role in primary research because surveys helps us to identify the key target audiences of the market. Additionally, surveys helps to identify the key target audience engaged with the market. Our survey team conducts the survey by targeting the key audience, thus gaining insights from them. Based on the perspectives of the customers, this information is utilized to formulate market strategies. Moreover, market surveys helps us to understand the current competitive situation of the industry. To be precise, our survey process typically involve with the 360 analysis of the market. This analytical process begins by identifying the prospective customers for a product or service related to the market/industry to obtain data on how a product/service could fit into customers’ lives.

Secondary Research: The secondary data sources includes information published by the on-profit organizations such as World bank, WHO, company fillings, investor presentations, annual reports, national government documents, statistical databases, blogs, articles, white papers and others. From the annual report, we analyse a company’s revenue to understand the key segment and market share of that organization in a particular region. We analyse the company websites and adopt the product mapping technique which is important for deriving the segment revenue. In the product mapping method, we select and categorize the products offered by the companies catering to domain specific market, deduce the product revenue for each of the companies so as to get overall estimation of the market size. We also source data and analyses trends based on information received from supply side and demand side intermediaries in the value chain. The supply side denotes the data gathered from supplier, distributor, wholesaler and the demand side illustrates the data gathered from the end customers for respective market domain.

The supply side for a domain specific market is analysed by:

The demand side for the market is estimated through:

In-house Library: Apart from these third-party sources, we have our in-house library of qualitative and quantitative information. Our in-house database includes market data for various industry and domains. These data are updated on regular basis as per the changing market scenario. Our library includes, historic databases, internal audit reports and archives.

Sometimes there are instances where there is no metadata or raw data available for any domain specific market. For those cases, we use our expertise to forecast and estimate the market size in order to generate comprehensive data sets. Our analyst team adopt a robust research technique in order to produce the estimates:

Data Synthesis: This stage involves the analysis & mapping of all the information obtained from the previous step. It also involves in scrutinizing the data for any discrepancy observed while data gathering related to the market. The data is collected with consideration to the heterogeneity of sources. Robust scientific techniques are in place for synthesizing disparate data sets and provide the essential contextual information that can orient market strategies. The Brainy Insights has extensive experience in data synthesis where the data passes through various stages:

Market Deduction & Formulation: The final stage comprises of assigning data points at appropriate market spaces so as to deduce feasible conclusions. Analyst perspective & subject matter expert based holistic form of market sizing coupled with industry analysis also plays a crucial role in this stage.

This stage involves in finalization of the market size and numbers that we have collected from data integration step. With data interpolation, it is made sure that there is no gap in the market data. Successful trend analysis is done by our analysts using extrapolation techniques, which provide the best possible forecasts for the market.

Data Validation & Market Feedback: Validation is the most important step in the process. Validation & re-validation via an intricately designed process helps us finalize data-points to be used for final calculations.

The Brainy Insights interacts with leading companies and experts of the concerned domain to develop the analyst team’s market understanding and expertise. It improves and substantiates every single data presented in the market reports. The data validation interview and discussion panels are typically composed of the most experienced industry members. The participants include, however, are not limited to:

Moreover, we always validate our data and findings through primary respondents from all the major regions we are working on.

Free Customization

Fortune 500 Clients

Free Yearly Update On Purchase Of Multi/Corporate License

Companies Served Till Date