- +1-315-215-1633

- sales@thebrainyinsights.com

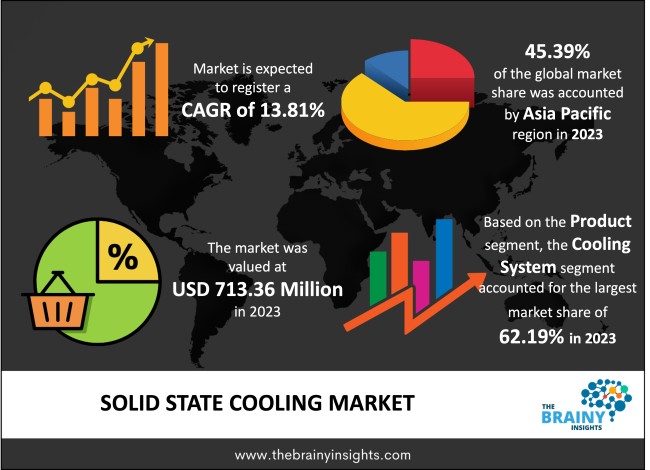

The global Solid State Cooling market generated USD 713.36 Million revenue in 2023 and is projected to grow at a CAGR of 13.81% from 2024 to 2033. The market is expected to reach USD 3,415.89 Million by 2033. The advancement in energy efficiency achieved through solid-state cooling technology is a pivotal factor propelling the growth of the global solid-state cooling market. Moreover, the escalation in infrastructure projects, rapid urban expansion, and industrial development, coupled with increased investments, contribute positively to the expansion of the solid-state cooling market. Furthermore, the growing adoption of solid-state cooling systems across various applications presents lucrative opportunities for market players in the forecast years.

Solid-state cooling is an innovative technology that utilizes the principles of thermoelectricity to achieve cooling effects without the need for traditional refrigeration systems. Unlike conventional cooling methods that rely on fluids or gases, solid-state cooling employs semiconductor materials to transfer heat from one side of the material to another when an electric current is applied. In solid-state cooling systems, thermoelectric modules are the central components. These modules are semiconductor materials, typically arranged in alternating n-type and p-type layers. When a direct current (DC) is passed through the module, it induces a temperature difference across the material, causing one side to become cooler (the cold side) and the other side to become warmer (the hot side). This phenomenon is known as the Peltier effect, and it forms the basis of solid-state cooling technology. One of the key advantages of solid-state cooling is its simplicity and reliability due to the absence of moving parts. This factor reduces maintenance requirements and increases the lifespan of the cooling system. Moreover, solid-state cooling systems can be more compact than traditional refrigeration systems, making them suitable for limited-space applications. Another advantage is the precise temperature control offered by solid-state cooling systems. The cooling effect can be precisely adjusted by varying the electric current applied to the thermoelectric modules, allowing for precise temperature regulation within a narrow range. This characteristic makes solid-state cooling excellent for applications where temperature stability is crucial, such as medical devices, electronic components, and laboratory equipment. Furthermore, solid-state cooling systems are environmentally friendly since they do not rely on refrigerants that can contribute to ozone depletion or global warming. This factor makes them a sustainable alternative to traditional cooling technologies. Overall, solid-state cooling represents a promising advancement in thermal management technology, offering simplicity, reliability, precise temperature control, and environmental sustainability across various applications.

Get an overview of this study by requesting a free sample

Miniaturization Trends - Solid-state cooling technologies have emerged as a viable option due to the demand for smaller, more efficient cooling solutions in various industries such as electronics, automotive, and healthcare. These technologies offer compact and lightweight solutions suitable for cooling smaller spaces or devices where traditional methods are impractical.

Energy Efficiency Concerns - Increasing concerns over energy consumption and environmental impact have spurred the adoption of energy-efficient cooling solutions. Solid-state cooling technologies, such as thermoelectric coolers, offer higher energy efficiency than conventional refrigeration systems, as they do not rely on harmful refrigerants and can provide precise temperature control.

Rising Demand in Electronics - The rapid growth of electronic devices, particularly in consumer electronics, telecommunications, and data centers, has driven the demand for efficient cooling solutions to manage heat dissipation. Solid-state cooling technologies offer faster response times, reduced maintenance, and silent operation, making them attractive for cooling sensitive electronic components.

High Initial Costs - One of the main obstacles to the expansive usage of solid-state cooling technologies is the relatively high upfront costs compared to traditional cooling methods. The initial investment required for implementing solid-state cooling solutions, which includes the purchase of thermoelectric modules and associated components, can be too much for some end-users, especially in cost-sensitive industries.

Temperature Differential Limitations - Thermoelectric cooling devices rely on the Peltier effect to make a difference in the temperature between the hot and cold sides of the module. However, thermoelectric material properties, current density, and heat transfer characteristics limit the achievable temperature differentials. This limitation affects solid-state cooling systems' cooling capacity and temperature range, restricting their suitability for applications that require extreme temperatures or high cooling loads.

Electronics Cooling - The rapid proliferation of electronic devices in diverse sectors, including telecommunications, consumer electronics, and automotive, creates a significant opportunity for solid-state cooling solutions. As electronic parts shrink more in size and increase in power density, the demand for compact and efficient cooling solutions becomes more pronounced. Solid-state cooling technologies, such as thermoelectric coolers and micro refrigerators, offer precise temperature control and compact form factors, making them well-suited for cooling electronics at the chip level or confined spaces.

Green Technology Adoption - With an increasing understanding of environmental sustainability and the importance of lowering CO2 emissions, there is growing interest in green cooling technologies. Solid-state cooling solutions, which eliminate the need for ozone-depleting refrigerants and have lower energy consumption than conventional vapour compression systems, are well-positioned to capitalize on this trend. Government incentives, environmental regulations, and corporate sustainability initiatives further drive the adoption of solid-state cooling technologies across various sectors, including commercial refrigeration, HVAC, and transportation.

Efficiency and Performance Optimization - Despite offering advantages such as energy efficiency and precise temperature control, solid-state cooling technologies face overall system efficiency and performance optimization challenges. Factors such as material properties, heat transfer mechanisms, and system design influence the efficiency and reliability of solid-state cooling devices. Achieving higher thermoelectric efficiency, reducing heat losses, and optimizing system integration are ongoing areas of research and development to enhance the performance of solid-state cooling solutions.

Material Availability and Reliability - The availability of high-performance thermoelectric materials in sufficient quantities and with consistent quality poses challenges for the widespread adoption of solid-state cooling technologies. Some advanced thermoelectric materials, such as skutterudites and half-Heusler compounds, are expensive to produce or require complex synthesis techniques, limiting their commercial viability. Moreover, ensuring the reliability and long-term stability of thermoelectric materials under various operating conditions is essential for the reliability and durability of solid-state cooling systems.

The regions analyzed for the market include North America, Europe, South America, Asia Pacific, the Middle East, and Africa. Asia Pacific emerged as the most prominent global Solid State Cooling market, with a 45.39% market revenue share in 2023.

Asia Pacific, particularly economies like Taiwan, China, South Korea, and Japan, is a global manufacturing hub for electronics, semiconductors, and other high-tech products. The region's advanced manufacturing capabilities, infrastructure, and skilled workforce make it a favourable location for producing solid-state cooling components and systems. The presence of established supply chains and manufacturing ecosystems enables companies in the region to produce and distribute solid-state cooling products at competitive prices efficiently. Most importantly, Asia Pacific is home to the world's leading technology companies, research institutions, and universities that drive innovation in solid-state cooling technologies. Countries like Japan and South Korea have a long history of research and development in electronics, materials science, and thermal management, leading to advancements in thermoelectric materials, device design, and system integration. The region's strong focus on innovation and collaboration fosters the development of cutting-edge solid-state cooling solutions tailored to various applications and industries. Moreover, the Asia Pacific region boasts a rapidly growing market for electronics and semiconductor devices, driven by urbanization, rising disposable incomes, and increasing demand for consumer electronics, smartphones, and automotive electronics. Solid-state cooling technologies find widespread application in cooling electronic components, data centers, and telecommunications infrastructure, catering to the needs of the region's expanding electronics market. The growing demand for compact, energy-efficient cooling solutions in electronics further drives the region's adoption of solid-state cooling technologies.

Asia Pacific Region Solid State Cooling Market Share in 2023 - 45.39%

www.thebrainyinsights.com

Check the geographical analysis of this market by requesting a free sample

The type segment is divided into single-stage, multi-stage and thermocycler. The single-stage segment dominated the market, with a share of around 51.27% in 2023. Single-stage solid-state cooling systems are simpler in design and construction than their multi-stage counterparts. They typically consist of a single thermoelectric module and require fewer components, resulting in lower manufacturing costs. This simplicity makes single-stage cooling systems more inexpensive and available to a broader range of applications and industries, driving their dominance in the market. Furthermore, single-stage solid-state cooling systems offer versatility and flexibility regarding temperature control and cooling capacity. They can be easily configured to achieve various temperature differentials and cooling capacities. This factor makes them suitable for various applications across industries, such as electronics cooling, automotive thermal management, and medical devices. The ability to tailor single-stage cooling systems to specific cooling requirements enhances their market appeal and adoption.

The product segment is classified into refrigeration system and cooling system. The cooling system segment dominated the market, with a share of around 62.19% in 2023. Cooling systems have undergone significant technological advancements, particularly in solid-state cooling. Innovations in thermoelectric materials, device design, system integration, and control algorithms have developed more efficient, reliable, and compact cooling solutions. These developments have extended the application range of cooling systems and enhanced their performance, making them increasingly attractive to end-users across industries. Moreover, with growing concerns over energy consumption and environmental sustainability, there is a heightened demand for energy-efficient cooling solutions that minimize power consumption and reduce greenhouse gas emissions. Cooling systems, particularly solid-state cooling technologies, offer advantages such as lower climate impact, higher energy efficiency, and elimination of harmful refrigerants compared to traditional vapour compression systems. These eco-friendly features contribute to the dominance of cooling systems in the solid-state cooling market, as they align with sustainability goals and regulatory requirements.

The end user segment includes automotive, consumer goods, medical, semiconductor and electronics, and others. The medical segment dominated the market, with a share of around 36.18% in 2023. The medical industry often requires precise temperature control for various applications such as medical imaging equipment, laboratory instrumentation, and temperature-sensitive drug storage. Solid-state cooling technologies offer precise and stable temperature control, ensuring medical devices' and procedures' accuracy and reliability. The ability of solid-state cooling systems to maintain tight temperature tolerances makes them indispensable in the medical field, driving their dominance in the market. Additionally, medical devices such as MRI machines, CT scanners, ultrasound equipment, and laser systems generate significant amounts of heat during operation. Effective thermal management is essential to dissipate heat and maintain optimal operating temperatures, ensuring the performance and longevity of medical devices. Solid-state cooling solutions, with their compactness, reliability, and silent operation, are well-suited for cooling medical devices in space-constrained environments such as hospitals, clinics, and laboratories.

| Attribute | Description |

|---|---|

| Market Size | Revenue (USD Million) |

| Market size value in 2023 | USD 713.36 Million |

| Market size value in 2033 | USD 3,415.89 Million |

| CAGR (2024 to 2033) | 13.81% |

| Historical data | 2020-2022 |

| Base Year | 2023 |

| Forecast | 2024-2033 |

| Region | The regions analyzed for the market are Asia Pacific, Europe, South America, North America, and Middle East & Africa. Furthermore, the regions are further analyzed at the country level. |

| Segments | Type, Product, and End User |

As per The Brainy Insights, the size of the solid state cooling market was valued at USD 713.36 million in 2023 to USD 3,415.89 million by 2033.

The global solid state cooling market is growing at a CAGR of 13.81% during the forecast period 2024-2033.

Asia Pacific became the largest market for solid state cooling.

Miniaturization trends and energy efficiency concerns drive the market's growth.

1. Introduction

1.1. Objectives of the Study

1.2. Market Definition

1.3. Research Scope

1.4. Currency

1.5. Key Target Audience

2. Research Methodology and Assumptions

3. Executive Summary

4. Premium Insights

4.1. Porter’s Five Forces Analysis

4.2. Value Chain Analysis

4.3. Top Investment Pockets

4.3.1. Market Attractiveness Analysis By Type

4.3.2. Market Attractiveness Analysis By Product

4.3.3. Market Attractiveness Analysis By End User

4.3.4. Market Attractiveness Analysis By Region

4.4. Industry Trends

5. Market Dynamics

5.1. Market Evaluation

5.2. Drivers

5.2.1. Miniaturization Trends

5.3. Restraints

5.3.1. High Initial Costs

5.4. Opportunities

5.4.1. The rapid proliferation of electronic devices

5.5. Challenges

5.5.1. Limited Cooling Capacity

6. Global Solid State Cooling Market Analysis and Forecast, By Type

6.1. Segment Overview

6.2. Single-Stage

6.3. Multi-Stage

6.4. Thermocycler

7. Global Solid State Cooling Market Analysis and Forecast, By Product

7.1. Segment Overview

7.2. Refrigeration System

7.3. Cooling System

8. Global Solid State Cooling Market Analysis and Forecast, By End User

8.1. Segment Overview

8.2. Automotive

8.3. Consumer Goods

8.4. Medical

8.5. Semiconductor and Electronics

8.6. Others

9. Global Solid State Cooling Market Analysis and Forecast, By Regional Analysis

9.1. Segment Overview

9.2. North America

9.2.1. U.S.

9.2.2. Canada

9.2.3. Mexico

9.3. Europe

9.3.1. Germany

9.3.2. France

9.3.3. U.K.

9.3.4. Italy

9.3.5. Spain

9.4. Asia-Pacific

9.4.1. Japan

9.4.2. China

9.4.3. India

9.5. South America

9.5.1. Brazil

9.6. Middle East and Africa

9.6.1. UAE

9.6.2. South Africa

10. Global Solid State Cooling Market-Competitive Landscape

10.1. Overview

10.2. Market Share of Key Players in the Solid State Cooling Market

10.2.1. Global Company Market Share

10.2.2. North America Company Market Share

10.2.3. Europe Company Market Share

10.2.4. APAC Company Market Share

10.3. Competitive Situations and Trends

10.3.1. Product Launches and Developments

10.3.2. Partnerships, Collaborations, and Agreements

10.3.3. Mergers & Acquisitions

10.3.4. Expansions

11. Company Profiles

11.1. Advanced Thermoelectric

11.1.1. Business Overview

11.1.2. Company Snapshot

11.1.3. Company Market Share Analysis

11.1.4. Company Product Portfolio

11.1.5. Recent Developments

11.1.6. SWOT Analysis

11.2. Align Sourcing

11.2.1. Business Overview

11.2.2. Company Snapshot

11.2.3. Company Market Share Analysis

11.2.4. Company Product Portfolio

11.2.5. Recent Developments

11.2.6. SWOT Analysis

11.3. AMS Technologies

11.3.1. Business Overview

11.3.2. Company Snapshot

11.3.3. Company Market Share Analysis

11.3.4. Company Product Portfolio

11.3.5. Recent Developments

11.3.6. SWOT Analysis

11.4. Crystal Ltd.

11.4.1. Business Overview

11.4.2. Company Snapshot

11.4.3. Company Market Share Analysis

11.4.4. Company Product Portfolio

11.4.5. Recent Developments

11.4.6. SWOT Analysis

11.5. Coherent Corp.

11.5.1. Business Overview

11.5.2. Company Snapshot

11.5.3. Company Market Share Analysis

11.5.4. Company Product Portfolio

11.5.5. Recent Developments

11.5.6. SWOT Analysis

11.6. CUI Devices

11.6.1. Business Overview

11.6.2. Company Snapshot

11.6.3. Company Market Share Analysis

11.6.4. Company Product Portfolio

11.6.5. Recent Developments

11.6.6. SWOT Analysis

11.7. Delta Electronics, Inc.

11.7.1. Business Overview

11.7.2. Company Snapshot

11.7.3. Company Market Share Analysis

11.7.4. Company Product Portfolio

11.7.5. Recent Developments

11.7.6. SWOT Analysis

11.8. Everredtronics

11.8.1. Business Overview

11.8.2. Company Snapshot

11.8.3. Company Market Share Analysis

11.8.4. Company Product Portfolio

11.8.5. Recent Developments

11.8.6. SWOT Analysis

11.9. Ferrotec

11.9.1. Business Overview

11.9.2. Company Snapshot

11.9.3. Company Market Share Analysis

11.9.4. Company Product Portfolio

11.9.5. Recent Developments

11.9.6. SWOT Analysis

11.10. Hicooltec Electronic

11.10.1. Business Overview

11.10.2. Company Snapshot

11.10.3. Company Market Share Analysis

11.10.4. Company Product Portfolio

11.10.5. Recent Developments

11.10.6. SWOT Analysis

11.11. Hi Z Technology

11.11.1. Business Overview

11.11.2. Company Snapshot

11.11.3. Company Market Share Analysis

11.11.4. Company Product Portfolio

11.11.5. Recent Developments

11.11.6. SWOT Analysis

11.12. Inheco Industrial Heating & Cooling

11.12.1. Business Overview

11.12.2. Company Snapshot

11.12.3. Company Market Share Analysis

11.12.4. Company Product Portfolio

11.12.5. Recent Developments

11.12.6. SWOT Analysis

11.13. Kelk Ltd.

11.13.1. Business Overview

11.13.2. Company Snapshot

11.13.3. Company Market Share Analysis

11.13.4. Company Product Portfolio

11.13.5. Recent Developments

11.13.6. SWOT Analysis

11.14. Kryotherm

11.14.1. Business Overview

11.14.2. Company Snapshot

11.14.3. Company Market Share Analysis

11.14.4. Company Product Portfolio

11.14.5. Recent Developments

11.14.6. SWOT Analysis

11.15. Komatsu Ltd.

11.15.1. Business Overview

11.15.2. Company Snapshot

11.15.3. Company Market Share Analysis

11.15.4. Company Product Portfolio

11.15.5. Recent Developments

11.15.6. SWOT Analysis

11.16. Laird Thermal Systems

11.16.1. Business Overview

11.16.2. Company Snapshot

11.16.3. Company Market Share Analysis

11.16.4. Company Product Portfolio

11.16.5. Recent Developments

11.16.6. SWOT Analysis

11.17. LG Innotek

11.17.1. Business Overview

11.17.2. Company Snapshot

11.17.3. Company Market Share Analysis

11.17.4. Company Product Portfolio

11.17.5. Recent Developments

11.17.6. SWOT Analysis

11.18. Merit Technology Group

11.18.1. Business Overview

11.18.2. Company Snapshot

11.18.3. Company Market Share Analysis

11.18.4. Company Product Portfolio

11.18.5. Recent Developments

11.18.6. SWOT Analysis

11.19. Micropelt

11.19.1. Business Overview

11.19.2. Company Snapshot

11.19.3. Company Market Share Analysis

11.19.4. Company Product Portfolio

11.19.5. Recent Developments

11.19.6. SWOT Analysis

11.20. O-Flexx Technologies

11.20.1. Business Overview

11.20.2. Company Snapshot

11.20.3. Company Market Share Analysis

11.20.4. Company Product Portfolio

11.20.5. Recent Developments

11.20.6. SWOT Analysis

11.21. P and N Technology Xiamen Co. Ltd.

11.21.1. Business Overview

11.21.2. Company Snapshot

11.21.3. Company Market Share Analysis

11.21.4. Company Product Portfolio

11.21.5. Recent Developments

11.21.6. SWOT Analysis

11.22. Phononic

11.22.1. Business Overview

11.22.2. Company Snapshot

11.22.3. Company Market Share Analysis

11.22.4. Company Product Portfolio

11.22.5. Recent Developments

11.22.6. SWOT Analysis

11.23. Sheetak

11.23.1. Business Overview

11.23.2. Company Snapshot

11.23.3. Company Market Share Analysis

11.23.4. Company Product Portfolio

11.23.5. Recent Developments

11.23.6. SWOT Analysis

11.24. Start-Up Ecosystem

11.24.1. Business Overview

11.24.2. Company Snapshot

11.24.3. Company Market Share Analysis

11.24.4. Company Product Portfolio

11.24.5. Recent Developments

11.24.6. SWOT Analysis

11.25. Solid State Cooling Systems

11.25.1. Business Overview

11.25.2. Company Snapshot

11.25.3. Company Market Share Analysis

11.25.4. Company Product Portfolio

11.25.5. Recent Developments

11.25.6. SWOT Analysis

11.26. TE Technology

11.26.1. Business Overview

11.26.2. Company Snapshot

11.26.3. Company Market Share Analysis

11.26.4. Company Product Portfolio

11.26.5. Recent Developments

11.26.6. SWOT Analysis

11.27. TEC Microsystems

11.27.1. Business Overview

11.27.2. Company Snapshot

11.27.3. Company Market Share Analysis

11.27.4. Company Product Portfolio

11.27.5. Recent Developments

11.27.6. SWOT Analysis

11.28. Thermion Company

11.28.1. Business Overview

11.28.2. Company Snapshot

11.28.3. Company Market Share Analysis

11.28.4. Company Product Portfolio

11.28.5. Recent Developments

11.28.6. SWOT Analysis

11.29. Thermonamic Electronics

11.29.1. Business Overview

11.29.2. Company Snapshot

11.29.3. Company Market Share Analysis

11.29.4. Company Product Portfolio

11.29.5. Recent Developments

11.29.6. SWOT Analysis

11.30. Wellen Technology

11.30.1. Business Overview

11.30.2. Company Snapshot

11.30.3. Company Market Share Analysis

11.30.4. Company Product Portfolio

11.30.5. Recent Developments

11.30.6. SWOT Analysis

List of Table

1. Global Solid State Cooling Market, By Type, 2020-2033 (USD Million) (K Units)

2. Global Single-Stage Solid State Cooling, Solid State Cooling Market, By Region, 2020-2033 (USD Million) (K Units)

3. Global Multi-Stage Solid State Cooling, Solid State Cooling Market, By Region, 2020-2033 (USD Million) (K Units)

4. Global Thermocycler Solid State Cooling, Solid State Cooling Market, By Region, 2020-2033 (USD Million) (K Units)

5. Global Solid State Cooling Market, By Product, 2020-2033 (USD Million) (K Units)

6. Global Refrigeration System Solid State Cooling Market, By Region, 2020-2033 (USD Million) (K Units)

7. Global Cooling System Solid State Cooling Market, By Region, 2020-2033 (USD Million) (K Units)

8. Global Solid State Cooling Market, By End User, 2020-2033 (USD Million) (K Units)

9. Global Automotive Solid State Cooling Market, By Region, 2020-2033 (USD Million) (K Units)

10. Global Consumer Goods Solid State Cooling Market, By Region, 2020-2033 (USD Million) (K Units)

11. Global Medical Solid State Cooling Market, By Region, 2020-2033 (USD Million) (K Units)

12. Global Semiconductor and Electronics Solid State Cooling Market, By Region, 2020-2033 (USD Million) (K Units)

13. Global Others, Solid State Cooling Market, By Region, 2020-2033 (USD Million) (K Units)

14. Global Solid State Cooling Market, By Region, 2020-2033 (USD Million) (K Units)

15. North America Solid State Cooling Market, By Type, 2020-2033 (USD Million) (K Units)

16. North America Solid State Cooling Market, By Product, 2020-2033 (USD Million) (K Units)

17. North America Solid State Cooling Market, By End User, 2020-2033 (USD Million) (K Units)

18. U.S. Solid State Cooling Market, By Type, 2020-2033 (USD Million) (K Units)

19. U.S. Solid State Cooling Market, By Product, 2020-2033 (USD Million) (K Units)

20. U.S. Solid State Cooling Market, By End User, 2020-2033 (USD Million) (K Units)

21. Canada Solid State Cooling Market, By Type, 2020-2033 (USD Million) (K Units)

22. Canada Solid State Cooling Market, By Product, 2020-2033 (USD Million) (K Units)

23. Canada Solid State Cooling Market, By End User, 2020-2033 (USD Million) (K Units)

24. Mexico Solid State Cooling Market, By Type, 2020-2033 (USD Million) (K Units)

25. Mexico Solid State Cooling Market, By Product, 2020-2033 (USD Million) (K Units)

26. Mexico Solid State Cooling Market, By End User, 2020-2033 (USD Million) (K Units)

27. Europe Solid State Cooling Market, By Type, 2020-2033 (USD Million) (K Units)

28. Europe Solid State Cooling Market, By Product, 2020-2033 (USD Million) (K Units)

29. Europe Solid State Cooling Market, By End User, 2020-2033 (USD Million) (K Units)

30. Germany Solid State Cooling Market, By Type, 2020-2033 (USD Million) (K Units)

31. Germany Solid State Cooling Market, By Product, 2020-2033 (USD Million) (K Units)

32. Germany Solid State Cooling Market, By End User, 2020-2033 (USD Million) (K Units)

33. France Solid State Cooling Market, By Type, 2020-2033 (USD Million) (K Units)

34. France Solid State Cooling Market, By Product, 2020-2033 (USD Million) (K Units)

35. France Solid State Cooling Market, By End User, 2020-2033 (USD Million) (K Units)

36. U.K. Solid State Cooling Market, By Type, 2020-2033 (USD Million) (K Units)

37. U.K. Solid State Cooling Market, By Product, 2020-2033 (USD Million) (K Units)

38. U.K. Solid State Cooling Market, By End User, 2020-2033 (USD Million) (K Units)

39. Italy Solid State Cooling Market, By Type, 2020-2033 (USD Million) (K Units)

40. Italy Solid State Cooling Market, By Product, 2020-2033 (USD Million) (K Units)

41. Italy Solid State Cooling Market, By End User, 2020-2033 (USD Million) (K Units)

42. Spain Solid State Cooling Market, By Type, 2020-2033 (USD Million) (K Units)

43. Spain Solid State Cooling Market, By Product, 2020-2033 (USD Million) (K Units)

44. Spain Solid State Cooling Market, By End User, 2020-2033 (USD Million) (K Units)

45. Asia Pacific Solid State Cooling Market, By Type, 2020-2033 (USD Million) (K Units)

46. Asia Pacific Solid State Cooling Market, By Product, 2020-2033 (USD Million) (K Units)

47. Asia Pacific Solid State Cooling Market, By End User, 2020-2033 (USD Million) (K Units)

48. Japan Solid State Cooling Market, By Type, 2020-2033 (USD Million) (K Units)

49. Japan Solid State Cooling Market, By Product, 2020-2033 (USD Million) (K Units)

50. Japan Solid State Cooling Market, By End User, 2020-2033 (USD Million) (K Units)

51. China Solid State Cooling Market, By Type, 2020-2033 (USD Million) (K Units)

52. China Solid State Cooling Market, By Product, 2020-2033 (USD Million) (K Units)

53. China Solid State Cooling Market, By End User, 2020-2033 (USD Million) (K Units)

54. India Solid State Cooling Market, By Type, 2020-2033 (USD Million) (K Units)

55. India Solid State Cooling Market, By Product, 2020-2033 (USD Million) (K Units)

56. India Solid State Cooling Market, By End User, 2020-2033 (USD Million) (K Units)

57. South America Solid State Cooling Market, By Type, 2020-2033 (USD Million) (K Units)

58. South America Solid State Cooling Market, By Product, 2020-2033 (USD Million) (K Units)

59. South America Solid State Cooling Market, By End User, 2020-2033 (USD Million) (K Units)

60. Brazil Solid State Cooling Market, By Type, 2020-2033 (USD Million) (K Units)

61. Brazil Solid State Cooling Market, By Product, 2020-2033 (USD Million) (K Units)

62. Brazil Solid State Cooling Market, By End User, 2020-2033 (USD Million) (K Units)

63. Middle East and Africa Solid State Cooling Market, By Type, 2020-2033 (USD Million) (K Units)

64. Middle East and Africa Solid State Cooling Market, By Product, 2020-2033 (USD Million) (K Units)

65. Middle East and Africa Solid State Cooling Market, By End User, 2020-2033 (USD Million) (K Units)

66. UAE Solid State Cooling Market, By Type, 2020-2033 (USD Million) (K Units)

67. UAE Solid State Cooling Market, By Product, 2020-2033 (USD Million) (K Units)

68. UAE Solid State Cooling Market, By End User, 2020-2033 (USD Million) (K Units)

69. South Africa Solid State Cooling Market, By Type, 2020-2033 (USD Million) (K Units)

70. South Africa Solid State Cooling Market, By Product, 2020-2033 (USD Million) (K Units)

71. South Africa Solid State Cooling Market, By End User, 2020-2033 (USD Million) (K Units)

List of Figures

1. Global Solid State Cooling Market Segmentation

2. Solid State Cooling Market: Research Methodology

3. Market Size Estimation Methodology: Bottom-Up Approach

4. Market Size Estimation Methodology: Top-Down Approach

5. Data Triangulation

6. Porter’s Five Forces Analysis

7. Value Chain Analysis

8. Global Solid State Cooling Market Attractiveness Analysis By Type

9. Global Solid State Cooling Market Attractiveness Analysis By Product

10. Global Solid State Cooling Market Attractiveness Analysis By End User

11. Global Solid State Cooling Market Attractiveness Analysis by Region

12. Global Solid State Cooling Market: Dynamics

13. Global Solid State Cooling Market Share By Type (2024 & 2033)

14. Global Solid State Cooling Market Share By Product (2024 & 2033)

15. Global Solid State Cooling Market Share By End User (2024 & 2033)

16. Global Solid State Cooling Market Share by Regions (2024 & 2033)

17. Global Solid State Cooling Market Share by Company (2023)

This study forecasts revenue at global, regional, and country levels from 2020 to 2033. The Brainy Insights has segmented the global Solid State Cooling market based on below-mentioned segments:

Global Solid State Cooling Market by Type:

Global Solid State Cooling Market by Product:

Global Solid State Cooling Market by End User:

Global Solid State Cooling Market by Region:

Research has its special purpose to undertake marketing efficiently. In this competitive scenario, businesses need information across all industry verticals; the information about customer wants, market demand, competition, industry trends, distribution channels etc. This information needs to be updated regularly because businesses operate in a dynamic environment. Our organization, The Brainy Insights incorporates scientific and systematic research procedures in order to get proper market insights and industry analysis for overall business success. The analysis consists of studying the market from a miniscule level wherein we implement statistical tools which helps us in examining the data with accuracy and precision.

Our research reports feature both; quantitative and qualitative aspects for any market. Qualitative information for any market research process are fundamental because they reveal the customer needs and wants, usage and consumption for any product/service related to a specific industry. This in turn aids the marketers/investors in knowing certain perceptions of the customers. Qualitative research can enlighten about the different product concepts and designs along with unique service offering that in turn, helps define marketing problems and generate opportunities. On the other hand, quantitative research engages with the data collection process through interviews, e-mail interactions, surveys and pilot studies. Quantitative aspects for the market research are useful to validate the hypotheses generated during qualitative research method, explore empirical patterns in the data with the help of statistical tools, and finally make the market estimations.

The Brainy Insights offers comprehensive research and analysis, based on a wide assortment of factual insights gained through interviews with CXOs and global experts and secondary data from reliable sources. Our analysts and industry specialist assume vital roles in building up statistical tools and analysis models, which are used to analyse the data and arrive at accurate insights with exceedingly informative research discoveries. The data provided by our organization have proven precious to a diverse range of companies, facilitating them to address issues such as determining which products/services are the most appealing, whether or not customers use the product in the manner anticipated, the purchasing intentions of the market and many others.

Our research methodology encompasses an idyllic combination of primary and secondary initiatives. Key phases involved in this process are listed below:

The phase involves the gathering and collecting of market data and its related information with the help of different sources & research procedures.

The data procurement stage involves in data gathering and collecting through various data sources.

This stage involves in extensive research. These data sources includes:

Purchased Database: Purchased databases play a crucial role in estimating the market sizes irrespective of the domain. Our purchased database includes:

Primary Research: The Brainy Insights interacts with leading companies and experts of the concerned domain to develop the analyst team’s market understanding and expertise. It improves and substantiates every single data presented in the market reports. Primary research mainly involves in telephonic interviews, E-mail interactions and face-to-face interviews with the raw material providers, manufacturers/producers, distributors, & independent consultants. The interviews that we conduct provides valuable data on market size and industry growth trends prevailing in the market. Our organization also conducts surveys with the various industry experts in order to gain overall insights of the industry/market. For instance, in healthcare industry we conduct surveys with the pharmacists, doctors, surgeons and nurses in order to gain insights and key information of a medical product/device/equipment which the customers are going to usage. Surveys are conducted in the form of questionnaire designed by our own analyst team. Surveys plays an important role in primary research because surveys helps us to identify the key target audiences of the market. Additionally, surveys helps to identify the key target audience engaged with the market. Our survey team conducts the survey by targeting the key audience, thus gaining insights from them. Based on the perspectives of the customers, this information is utilized to formulate market strategies. Moreover, market surveys helps us to understand the current competitive situation of the industry. To be precise, our survey process typically involve with the 360 analysis of the market. This analytical process begins by identifying the prospective customers for a product or service related to the market/industry to obtain data on how a product/service could fit into customers’ lives.

Secondary Research: The secondary data sources includes information published by the on-profit organizations such as World bank, WHO, company fillings, investor presentations, annual reports, national government documents, statistical databases, blogs, articles, white papers and others. From the annual report, we analyse a company’s revenue to understand the key segment and market share of that organization in a particular region. We analyse the company websites and adopt the product mapping technique which is important for deriving the segment revenue. In the product mapping method, we select and categorize the products offered by the companies catering to domain specific market, deduce the product revenue for each of the companies so as to get overall estimation of the market size. We also source data and analyses trends based on information received from supply side and demand side intermediaries in the value chain. The supply side denotes the data gathered from supplier, distributor, wholesaler and the demand side illustrates the data gathered from the end customers for respective market domain.

The supply side for a domain specific market is analysed by:

The demand side for the market is estimated through:

In-house Library: Apart from these third-party sources, we have our in-house library of qualitative and quantitative information. Our in-house database includes market data for various industry and domains. These data are updated on regular basis as per the changing market scenario. Our library includes, historic databases, internal audit reports and archives.

Sometimes there are instances where there is no metadata or raw data available for any domain specific market. For those cases, we use our expertise to forecast and estimate the market size in order to generate comprehensive data sets. Our analyst team adopt a robust research technique in order to produce the estimates:

Data Synthesis: This stage involves the analysis & mapping of all the information obtained from the previous step. It also involves in scrutinizing the data for any discrepancy observed while data gathering related to the market. The data is collected with consideration to the heterogeneity of sources. Robust scientific techniques are in place for synthesizing disparate data sets and provide the essential contextual information that can orient market strategies. The Brainy Insights has extensive experience in data synthesis where the data passes through various stages:

Market Deduction & Formulation: The final stage comprises of assigning data points at appropriate market spaces so as to deduce feasible conclusions. Analyst perspective & subject matter expert based holistic form of market sizing coupled with industry analysis also plays a crucial role in this stage.

This stage involves in finalization of the market size and numbers that we have collected from data integration step. With data interpolation, it is made sure that there is no gap in the market data. Successful trend analysis is done by our analysts using extrapolation techniques, which provide the best possible forecasts for the market.

Data Validation & Market Feedback: Validation is the most important step in the process. Validation & re-validation via an intricately designed process helps us finalize data-points to be used for final calculations.

The Brainy Insights interacts with leading companies and experts of the concerned domain to develop the analyst team’s market understanding and expertise. It improves and substantiates every single data presented in the market reports. The data validation interview and discussion panels are typically composed of the most experienced industry members. The participants include, however, are not limited to:

Moreover, we always validate our data and findings through primary respondents from all the major regions we are working on.

Free Customization

Fortune 500 Clients

Free Yearly Update On Purchase Of Multi/Corporate License

Companies Served Till Date