- +1-315-215-1633

- sales@thebrainyinsights.com

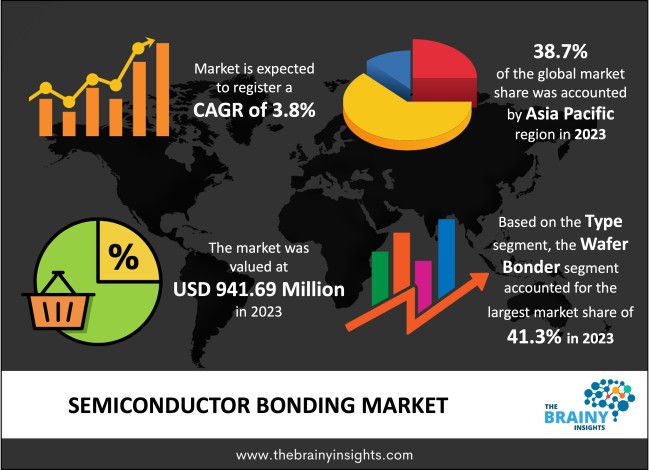

Semiconductor Bonding Market is expected to reach USD 1,367.35 million by 2033, at a CAGR of 3.8% from 2024 to 2033. The global increase in the adoption of IoT and AI in the automotive sector is a crucial factor driving the semiconductor bonding market. Semiconductors are essentially atoms that form a uniform structure through bonding. This type of bonding produces a homogeneous material with consistent properties throughout, making it ideal for creating integrated circuits and manufacturing devices. The demand for semiconductor ICs capable of performing multiple functions has risen as the complexity of designs increases, driving market growth during the forecast period. To function correctly within an integrated chip, semiconductor bonding equipment must connect it to the printed circuitry or package using wire-bonding techniques such as die-bonding and dicing. These processes represent back-end steps in chip formation. The growing popularity of IoT devices and increased adoption rates among automated automotive components act synergistically towards boosting expansion prospects in this ever-growing market.

Semiconductors like Gallium Nitrate (GaN) are atoms interconnected in a regular and periodic pattern to form a structure whereby 8 electrons envelop each bit. Semiconductors are made up of combined atoms to develop a uniform framework. The object's framework is homogeneous, i.e., nearly identical across the bonding model. Semiconductor bonding is broadly used in constructing a variety of integrated circuits (ICs). The electrons that encircle each particle in a semiconductor have a chemical bond. When between two atoms, electrons are shared; a bond is a covalent bond. Each bit forms four covalent bonds with the four atoms surrounding it. The semiconductor industry is critical to the development of hybrid and electric vehicles. Power semiconductor devices including freewheeling diodes, voltage boost DC-DC converters, ICs, motor drives, MEMS, fuel cell air compressors, low-voltage power MOSFETs, and insulated gate bipolar transistors (IGBTs) are crucial parts in electric and hybrid vehicles. Therefore each atom and its four neighboring atoms share 8 electrons. Semiconductor connectivity is used to create cavities, composite 3D structures, and sealed liquid channels that are structurally and electrically strong. It is essential to connect two or more micro-components firmly.

Get an overview of this study by requesting a free sample

The growing use of piled die technology in IoT devices propels the semiconductor bonding market forward. Stacked die refers to the process of stacking one bare die on top of another within a single semiconductor package; it is used to use the same location area on a membrane for multiple functions. Die stacking improves electrochemical device characteristics because shorter connectivity routing between electronic circuits improves digital signals. The semiconductor industry's device manufacturers (OEMs) are concentrating on utilizing the concept of IoT beyond interconnection. Sensors, RFID tags, smart meters, intelligent signposts, and allocation control systems are among the IoT technologies and devices that are progressively being used in applications such as constructing and remote monitoring, advanced manufacturing, combined feature, intelligent department stores, intelligent transportation systems, and shipping, and so on. Semiconductor bonding methodologies are used in IoT devices to connect multi-stacked dies on surfaces while taking up as little space as possible.

Semiconductor bonding hardware is a piece of powerful machinery that requires a high input capacity to execute die-to-attach processes. The energy needed for this equipment ranges from hundreds or even thousands of watts. The cost of manufacturing semiconductor bonding machinery is also very high due to complex and expensive elements. To assemble various large and small parts, such as the screen, bond formation hand, vacuum, sensors, and heating element. As a result, semiconductor bonding hardware's overall manufacturing and shareholding expenses for die bonder machinery are generally high. Moreover, the enormous cost of semiconductor wafers raises the operational expenditures of semiconductor bonding, impeding market growth.

The increasing adoption of thin wafers in the semiconductor sector is a significant driver of the wafer bonding market's expansion. Thin wafer breakthroughs have aided in the elimination of many conventional fabrication processes. The narrow wafer sector is attracting Chinese IC producers looking to influence this technology to receive the benefits such as ultra-low energy usage and ultra-high electronic success. Many IC suppliers in China are currently motivated by fine chips with superior efficiency at lower processing voltage levels. Therefore, thin wafer innovations, including wafer bonding, are gaining popularity among Chinese IC makers.

Die bonder machinery uses physical activities to lift and move the die for the bonding process. Numerous mechanical components in the machinery necessitate high precision motion to connect the die to the material successfully. However, operating equipment can pulsate due to various issues, including destabilization and unusual movement of adhesive structures. Die misalignment or busting can occur due to resonance in die bonders. Mechanical part vibration has become a big challenge for semiconductor bonding device manufacturers, which must be resolved. Thin wafers are brittle and easily damaged by stress and pressure. A thin wafer is highly adaptable and can break even under light pressure or stress. Dies made from thin wafers can quickly destroy during the inbuilt wafer pruning procedure. Players are attempting to deal with uncertainties by creating support networks for handling thin wafers through multiple methods such as wafer bonding and debonding. In addition, the elevated adhesive is used in carriers that manage thin wafers.

The semiconductor bonding market has been segmented based on type, application and technology, and regions.

The regions analyzed for the market include North America, Europe, South America, Asia Pacific, the Middle East, and Africa. Asia Pacific region emerged as the largest market for the semiconductor bonding market with a 38.7% market share in 2023.

Asia Pacific region Semiconductor Bonding Market Share in 2023 - 38.7%

www.thebrainyinsights.com

Check the geographical analysis of this market by requesting a free sample

The key players are now concentrating on implementing strategies such as adopting new technology, product innovations, mergers & acquisitions, joint venture, alliances, and partnerships to improve their market position in the global semiconductor bonding market.

MicroTec SE formed a partnership with SET Corporation in September 2021 and provided customers with an automated, configurable, high-yield equipment solution.

ASM PACIFIC TECHNOLOGY (ASMPT) launched three new production systems in April 2021. It X-Micro-Transfer Celeprint's Printing (MTP) and ASM AMICRA's high accuracy die bonding techniques to develop the semiconductor industry's first complete platform that supports large volume heterogeneous assimilation of super-thin dies onto up to 300mm base wafers.

BE Semiconductor Industries NV (Besi) and Applied Materials, Inc. teamed up in October 2020 and created the industry's first comprehensive and conclusively demonstrated device solution for die-based hybrid bonding, an arising chip-to-chip connectivity technique that provides heterogeneous chip and subsystem designs for applications that require high computing, and 5G.

Panasonic Corporation collaborated with IBM Corporation in October 2019 to develop and market and sell a new high-value-added remedy that assists clients in improving their equipment efficiency and attaining higher manufacturing.

As per The Brainy Insights, the size of the Semiconductor Bonding market was valued at USD 941.69 Million in 2023 to USD 1,367.35 Million by 2033.

Global Semiconductor Bonding market is growing at a CAGR of 3.8% during the forecast period 2024-2033.

Asia Pacific region emerged as the largest market for the Semiconductor Bonding.

The market's growth will be influenced by the increase in adoption of IoT and AI in the automotive industry.

Expensive ownership could hamper the market growth.

China's IC industry is growing will provide huge opportunities to the market.

Key players are BE Semiconductor Industries NV, ASM Pacific Technology Ltd., Kulicke & Soffa, Panasonic, Fuji Corporation, Yamaha Motor Robotics Corporation Co., SUSS MicroTech SE, Shiaura Mechatronics.

1. Introduction

1.1. Objectives of the Study

1.2. Market Definition

1.3. Research Scope

1.4. Currency

1.5. Key Target Audience

2. Research Methodology and Assumptions

3. Executive Summary

4. Premium Insights

4.1. Porter’s Five Forces Analysis

4.2. Value Chain Analysis

4.3. Top Investment Pockets

4.3.1. Market Attractiveness Analysis By Type

4.3.2. Market Attractiveness Analysis By Application

4.3.3. Market Attractiveness Analysis By Technology

4.3.4. Market Attractiveness Analysis By Region

4.4. Industry Trends

5. Market Dynamics

5.1. Market Evaluation

5.2. Drivers

5.2.1. Increase in adoption of IoT and AI in the automotive industry

5.3. Restraints

5.3.1. Expensive Ownership

5.4. Opportunities

5.4.1. China's IC industry is growing

5.5. Challenges

5.5.1. Mechanical lack of balance of machine components

6. Global Semiconductor Bonding Market Analysis and Forecast, By Type

6.1. Segment Overview

6.2. Wafer Bonder

6.3. Flip Chip Bonder

6.4. Die Bonder

7. Global Semiconductor Bonding Market Analysis and Forecast, By Application

7.1. Segment Overview

7.2. CMOS Image Sensors

7.3. RF Devices

7.4. LED

7.5. 3D NAND

7.6. MEMS and Sensors

8. Global Semiconductor Bonding Market Analysis and Forecast, By Technology

8.1. Segment Overview

8.2. Die Bonding Technology

8.2.1. Flip-chip Attachment

8.2.2. Epoxy Die Bonding

8.2.3. Hybrid Bonding

8.2.4. Eutectic Die Bonding

8.3. Wafer Bonding Technology

8.3.1. TCB Wafer Bonding

8.3.2. Direct Wafer Bonding

8.3.3. Hybrid Bonding

8.3.4. Anodic Wafer Bonding)

9. Global Semiconductor Bonding Market Analysis and Forecast, By Regional Analysis

9.1. Segment Overview

9.2. North America

9.2.1. U.S.

9.2.2. Canada

9.2.3. Mexico

9.3. Europe

9.3.1. Germany

9.3.2. France

9.3.3. U.K.

9.3.4. Italy

9.3.5. Spain

9.4. Asia-Pacific

9.4.1. Japan

9.4.2. China

9.4.3. India

9.5. South America

9.5.1. Brazil

9.6. Middle East and Africa

9.6.1. UAE

9.6.2. South Africa

10. Global Semiconductor Bonding Market-Competitive Landscape

10.1. Overview

10.2. Market Share of Key Players in the Semiconductor Bonding Market

10.2.1. Global Company Market Share

10.2.2. North America Company Market Share

10.2.3. Europe Company Market Share

10.2.4. APAC Company Market Share

10.3. Competitive Situations and Trends

10.3.1. Product Launches and Developments

10.3.2. Partnerships, Collaborations, and Agreements

10.3.3. Mergers & Acquisitions

10.3.4. Expansions

11. Company Profiles

11.1. BE Semiconductor Industries NV

11.1.1. Business Overview

11.1.2. Company Snapshot

11.1.3. Company Market Share Analysis

11.1.4. Company Component Portfolio

11.1.5. Recent Developments

11.1.6. SWOT Analysis

11.2. ASM Pacific Technology Ltd.

11.2.1. Business Overview

11.2.2. Company Snapshot

11.2.3. Company Market Share Analysis

11.2.4. Company Component Portfolio

11.2.5. Recent Developments

11.2.6. SWOT Analysis

11.3. Kulicke & Soffa

11.3.1. Business Overview

11.3.2. Company Snapshot

11.3.3. Company Market Share Analysis

11.3.4. Company Component Portfolio

11.3.5. Recent Developments

11.3.6. SWOT Analysis

11.4. Panasonic

11.4.1. Business Overview

11.4.2. Company Snapshot

11.4.3. Company Market Share Analysis

11.4.4. Company Component Portfolio

11.4.5. Recent Developments

11.4.6. SWOT Analysis

11.5. Fuji Corporation

11.5.1. Business Overview

11.5.2. Company Snapshot

11.5.3. Company Market Share Analysis

11.5.4. Company Component Portfolio

11.5.5. Recent Developments

11.5.6. SWOT Analysis

11.6. SUSS MicroTech SE

11.6.1. Business Overview

11.6.2. Company Snapshot

11.6.3. Company Market Share Analysis

11.6.4. Company Component Portfolio

11.6.5. Recent Developments

11.6.6. SWOT Analysis

11.7. Shiaura Mechatronics

11.7.1. Business Overview

11.7.2. Company Snapshot

11.7.3. Company Market Share Analysis

11.7.4. Company Component Portfolio

11.7.5. Recent Developments

11.7.6. SWOT Analysis

List of Table

1. Global Semiconductor Bonding Market, By Type, 2020-2033 (USD Million)

2. Global Wafer Bonder Semiconductor Bonding Market, By Region, 2020-2033 (USD Million)

3. Global Flip Chip Bonder Semiconductor Bonding Market, By Region, 2020-2033 (USD Million)

4. Global Die Bonder Semiconductor Bonding Market, By Region, 2020-2033 (USD Million)

5. Global Semiconductor Bonding Market, By Application, 2020-2033 (USD Million)

6. Global CMOS Image Sensors Semiconductor Bonding Market, By Region, 2020-2033 (USD Million)

7. Global LED Semiconductor Bonding Market, By Region, 2020-2033 (USD Million)

8. Global 3D NAND Semiconductor Bonding Market, By Region, 2020-2033 (USD Million)

9. Global MEMS and Sensors Semiconductor Bonding Market, By Region, 2020-2033 (USD Million)

10. Global Semiconductor Bonding Market, By Technology, 2020-2033 (USD Million)

11. Global Die Bonding Technology Semiconductor Bonding Market, By Region, 2020-2033 (USD Million)

12. Global Wafer Bonding TechnologySemiconductor Bonding Market, By Region, 2020-2033 (USD Million)

13. Global Semiconductor Bonding Market, By Region, 2020-2033 (USD Million)

14. North America Semiconductor Bonding Market, By Type, 2020-2033 (USD Million)

15. North America Semiconductor Bonding Market, By Application, 2020-2033 (USD Million)

16. North America Semiconductor Bonding Market, By Technology, 2020-2033 (USD Million)

17. U.S. Semiconductor Bonding Market, By Type, 2020-2033 (USD Million)

18. U.S. Semiconductor Bonding Market, By Application, 2020-2033 (USD Million)

19. U.S. Semiconductor Bonding Market, By Technology, 2020-2033 (USD Million)

20. Canada Semiconductor Bonding Market, By Type, 2020-2033 (USD Million)

21. Canada Semiconductor Bonding Market, By Application, 2020-2033 (USD Million)

22. Canada Semiconductor Bonding Market, By Technology, 2020-2033 (USD Million)

23. Mexico Semiconductor Bonding Market, By Type, 2020-2033 (USD Million)

24. Mexico Semiconductor Bonding Market, By Application, 2020-2033 (USD Million)

25. Mexico Semiconductor Bonding Market, By Technology, 2020-2033 (USD Million)

26. Europe Semiconductor Bonding Market, By Type, 2020-2033 (USD Million)

27. Europe Semiconductor Bonding Market, By Application, 2020-2033 (USD Million)

28. Europe Semiconductor Bonding Market, By Technology, 2020-2033 (USD Million)

29. Germany Semiconductor Bonding Market, By Type, 2020-2033 (USD Million)

30. Germany Semiconductor Bonding Market, By Application, 2020-2033 (USD Million)

31. Germany Semiconductor Bonding Market, By Technology, 2020-2033 (USD Million)

32. France Semiconductor Bonding Market, By Type, 2020-2033 (USD Million)

33. France Semiconductor Bonding Market, By Application, 2020-2033 (USD Million)

34. France Semiconductor Bonding Market, By Technology, 2020-2033 (USD Million)

35. U.K. Semiconductor Bonding Market, By Type, 2020-2033 (USD Million)

36. U.K. Semiconductor Bonding Market, By Application, 2020-2033 (USD Million)

37. U.K. Semiconductor Bonding Market, By Technology, 2020-2033 (USD Million)

38. Italy Semiconductor Bonding Market, By Type, 2020-2033 (USD Million)

39. Italy Semiconductor Bonding Market, By Application, 2020-2033 (USD Million)

40. Italy Semiconductor Bonding Market, By Technology, 2020-2033 (USD Million)

41. Spain Semiconductor Bonding Market, By Type, 2020-2033 (USD Million)

42. Spain Semiconductor Bonding Market, By Application, 2020-2033 (USD Million)

43. Spain Semiconductor Bonding Market, By Technology, 2020-2033 (USD Million)

44. Asia Pacific Semiconductor Bonding Market, By Type, 2020-2033 (USD Million)

45. Asia Pacific Semiconductor Bonding Market, By Application, 2020-2033 (USD Million)

46. Asia Pacific Semiconductor Bonding Market, By Technology, 2020-2033 (USD Million)

47. Japan Semiconductor Bonding Market, By Type, 2020-2033 (USD Million)

48. Japan Semiconductor Bonding Market, By Application, 2020-2033 (USD Million)

49. Japan Semiconductor Bonding Market, By Technology, 2020-2033 (USD Million)

50. China Semiconductor Bonding Market, By Type, 2020-2033 (USD Million)

51. China Semiconductor Bonding Market, By Application, 2020-2033 (USD Million)

52. China Semiconductor Bonding Market, By Technology, 2020-2033 (USD Million)

53. India Semiconductor Bonding Market, By Type, 2020-2033 (USD Million)

54. India Semiconductor Bonding Market, By Application, 2020-2033 (USD Million)

55. India Semiconductor Bonding Market, By Technology, 2020-2033 (USD Million)

56. South America Semiconductor Bonding Market, By Type, 2020-2033 (USD Million)

57. South America Semiconductor Bonding Market, By Application, 2020-2033 (USD Million)

58. South America Semiconductor Bonding Market, By Technology, 2020-2033 (USD Million)

59. Brazil Semiconductor Bonding Market, By Type, 2020-2033 (USD Million)

60. Brazil Semiconductor Bonding Market, By Application, 2020-2033 (USD Million)

61. Brazil Semiconductor Bonding Market, By Technology, 2020-2033 (USD Million)

62. Middle East and Africa Semiconductor Bonding Market, By Type, 2020-2033 (USD Million)

63. Middle East and Africa Semiconductor Bonding Market, By Application, 2020-2033 (USD Million)

64. Middle East and Africa Semiconductor Bonding Market, By Technology, 2020-2033 (USD Million)

65. UAE Semiconductor Bonding Market, By Type, 2020-2033 (USD Million)

66. UAE Semiconductor Bonding Market, By Application, 2020-2033 (USD Million)

67. UAE Semiconductor Bonding Market, By Technology, 2020-2033 (USD Million)

68. South Africa Semiconductor Bonding Market, By Type, 2020-2033 (USD Million)

69. South Africa Semiconductor Bonding Market, By Application, 2020-2033 (USD Million)

70. South Africa Semiconductor Bonding Market, By Technology, 2020-2033 (USD Million)

List of Figures

1. Global Semiconductor Bonding Market Segmentation

2. Semiconductor Bonding Market: Research Methodology

3. Market Size Estimation Methodology: Bottom-Up Approach

4. Market Size Estimation Methodology: Top-Down Approach

5. Data Triangulation

6. Porter’s Five Forces Analysis

7. Value Chain Analysis

8. Global Semiconductor Bonding Market Attractiveness Analysis By Type

9. Global Semiconductor Bonding Market Attractiveness Analysis By Application

10. Global Semiconductor Bonding Market Attractiveness Analysis By Technology

11. Global Semiconductor Bonding Market Attractiveness Analysis By Region

12. Global Semiconductor Bonding Market: Dynamics

13. Global Semiconductor Bonding Market Share by Type (2023 & 2033)

14. Global Semiconductor Bonding Market Share by Application (2023 & 2033)

15. Global Semiconductor Bonding Market Share by Technology (2023 & 2033)

16. Global Semiconductor Bonding Market Share by Regions (2023 & 2033)

17. Global Semiconductor Bonding Market Share by Company (2023)

This study forecasts revenue at global, regional, and country levels from 2020 to 2033. The Brainy Insights has segmented the global semiconductor bonding market based on below mentioned segments:

Global Semiconductor Bonding Market by Type:

Global Semiconductor Bonding Market by Application:

Global Semiconductor Bonding Market by Technology:

Global Semiconductor Bonding Market by Region:

Research has its special purpose to undertake marketing efficiently. In this competitive scenario, businesses need information across all industry verticals; the information about customer wants, market demand, competition, industry trends, distribution channels etc. This information needs to be updated regularly because businesses operate in a dynamic environment. Our organization, The Brainy Insights incorporates scientific and systematic research procedures in order to get proper market insights and industry analysis for overall business success. The analysis consists of studying the market from a miniscule level wherein we implement statistical tools which helps us in examining the data with accuracy and precision.

Our research reports feature both; quantitative and qualitative aspects for any market. Qualitative information for any market research process are fundamental because they reveal the customer needs and wants, usage and consumption for any product/service related to a specific industry. This in turn aids the marketers/investors in knowing certain perceptions of the customers. Qualitative research can enlighten about the different product concepts and designs along with unique service offering that in turn, helps define marketing problems and generate opportunities. On the other hand, quantitative research engages with the data collection process through interviews, e-mail interactions, surveys and pilot studies. Quantitative aspects for the market research are useful to validate the hypotheses generated during qualitative research method, explore empirical patterns in the data with the help of statistical tools, and finally make the market estimations.

The Brainy Insights offers comprehensive research and analysis, based on a wide assortment of factual insights gained through interviews with CXOs and global experts and secondary data from reliable sources. Our analysts and industry specialist assume vital roles in building up statistical tools and analysis models, which are used to analyse the data and arrive at accurate insights with exceedingly informative research discoveries. The data provided by our organization have proven precious to a diverse range of companies, facilitating them to address issues such as determining which products/services are the most appealing, whether or not customers use the product in the manner anticipated, the purchasing intentions of the market and many others.

Our research methodology encompasses an idyllic combination of primary and secondary initiatives. Key phases involved in this process are listed below:

The phase involves the gathering and collecting of market data and its related information with the help of different sources & research procedures.

The data procurement stage involves in data gathering and collecting through various data sources.

This stage involves in extensive research. These data sources includes:

Purchased Database: Purchased databases play a crucial role in estimating the market sizes irrespective of the domain. Our purchased database includes:

Primary Research: The Brainy Insights interacts with leading companies and experts of the concerned domain to develop the analyst team’s market understanding and expertise. It improves and substantiates every single data presented in the market reports. Primary research mainly involves in telephonic interviews, E-mail interactions and face-to-face interviews with the raw material providers, manufacturers/producers, distributors, & independent consultants. The interviews that we conduct provides valuable data on market size and industry growth trends prevailing in the market. Our organization also conducts surveys with the various industry experts in order to gain overall insights of the industry/market. For instance, in healthcare industry we conduct surveys with the pharmacists, doctors, surgeons and nurses in order to gain insights and key information of a medical product/device/equipment which the customers are going to usage. Surveys are conducted in the form of questionnaire designed by our own analyst team. Surveys plays an important role in primary research because surveys helps us to identify the key target audiences of the market. Additionally, surveys helps to identify the key target audience engaged with the market. Our survey team conducts the survey by targeting the key audience, thus gaining insights from them. Based on the perspectives of the customers, this information is utilized to formulate market strategies. Moreover, market surveys helps us to understand the current competitive situation of the industry. To be precise, our survey process typically involve with the 360 analysis of the market. This analytical process begins by identifying the prospective customers for a product or service related to the market/industry to obtain data on how a product/service could fit into customers’ lives.

Secondary Research: The secondary data sources includes information published by the on-profit organizations such as World bank, WHO, company fillings, investor presentations, annual reports, national government documents, statistical databases, blogs, articles, white papers and others. From the annual report, we analyse a company’s revenue to understand the key segment and market share of that organization in a particular region. We analyse the company websites and adopt the product mapping technique which is important for deriving the segment revenue. In the product mapping method, we select and categorize the products offered by the companies catering to domain specific market, deduce the product revenue for each of the companies so as to get overall estimation of the market size. We also source data and analyses trends based on information received from supply side and demand side intermediaries in the value chain. The supply side denotes the data gathered from supplier, distributor, wholesaler and the demand side illustrates the data gathered from the end customers for respective market domain.

The supply side for a domain specific market is analysed by:

The demand side for the market is estimated through:

In-house Library: Apart from these third-party sources, we have our in-house library of qualitative and quantitative information. Our in-house database includes market data for various industry and domains. These data are updated on regular basis as per the changing market scenario. Our library includes, historic databases, internal audit reports and archives.

Sometimes there are instances where there is no metadata or raw data available for any domain specific market. For those cases, we use our expertise to forecast and estimate the market size in order to generate comprehensive data sets. Our analyst team adopt a robust research technique in order to produce the estimates:

Data Synthesis: This stage involves the analysis & mapping of all the information obtained from the previous step. It also involves in scrutinizing the data for any discrepancy observed while data gathering related to the market. The data is collected with consideration to the heterogeneity of sources. Robust scientific techniques are in place for synthesizing disparate data sets and provide the essential contextual information that can orient market strategies. The Brainy Insights has extensive experience in data synthesis where the data passes through various stages:

Market Deduction & Formulation: The final stage comprises of assigning data points at appropriate market spaces so as to deduce feasible conclusions. Analyst perspective & subject matter expert based holistic form of market sizing coupled with industry analysis also plays a crucial role in this stage.

This stage involves in finalization of the market size and numbers that we have collected from data integration step. With data interpolation, it is made sure that there is no gap in the market data. Successful trend analysis is done by our analysts using extrapolation techniques, which provide the best possible forecasts for the market.

Data Validation & Market Feedback: Validation is the most important step in the process. Validation & re-validation via an intricately designed process helps us finalize data-points to be used for final calculations.

The Brainy Insights interacts with leading companies and experts of the concerned domain to develop the analyst team’s market understanding and expertise. It improves and substantiates every single data presented in the market reports. The data validation interview and discussion panels are typically composed of the most experienced industry members. The participants include, however, are not limited to:

Moreover, we always validate our data and findings through primary respondents from all the major regions we are working on.

Free Customization

Fortune 500 Clients

Free Yearly Update On Purchase Of Multi/Corporate License

Companies Served Till Date