- +1-315-215-1633

- sales@thebrainyinsights.com

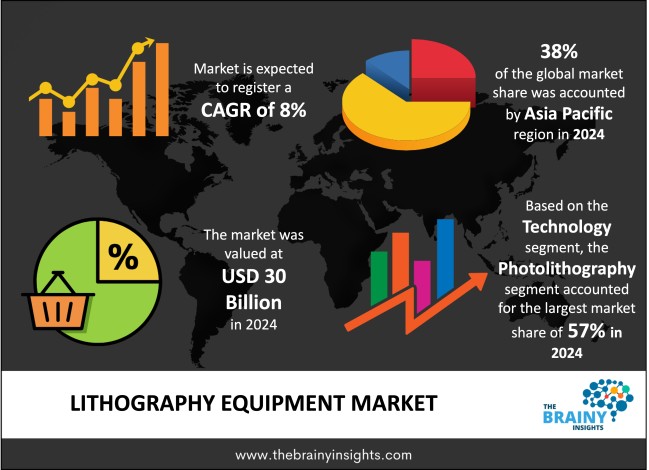

The global lithography equipment market was valued at USD 30 billion in 2024 and grew at a CAGR of 8% from 2025 to 2034. The market is expected to reach USD 64.76 billion by 2034. The increasing demand for consumer electronics will drive the growth of the global lithography equipment market.

Semiconductor manufacturing depends on lithography equipment to produce integrated circuits (ICs). The lithographic procedure serves as a vital semiconductor wafer processing method which results in small and complex electronic features of current devices. The main purpose of lithography equipment consists of photo-exposing patterns through light on wafer-based photosensitive layers before developing and etching them to form circuits. Photolithography systems represented by steppers and scanners function with ultraviolet (UV) light to carry out pattern projection. Proper steppers direct illumination to one wafer each time but scanners utilize optical lenses to accomplish step-by-step pattern printing across entire wafers with increased operational efficiency. The systems maintain precise alignment because deviations however minor will result in defective circuit performance. The production of advanced and miniature ICs depends heavily on precise lithography equipment resolution together with accuracy which makes extreme ultraviolet (EUV) lithography technology advancement essential. EUV technology produces narrower light wavelength frequencies which enables manufacturers to generate crucial features needed for contemporary microprocessors and memory chips. The future growth of microelectronics depends heavily on lithography technology because manufacturers need advanced printing solutions to achieve improving devices that are more powerful while smaller in size.

Get an overview of this study by requesting a free sample

The increasing demand for consumer electronics – The increased need for consumer electronics is the main reason behind the increased need for improved lithography equipment. Companies focused on consumer electronics seek to develop devices that will achieve better processing efficiency combined with improved battery endurance and enhanced connectivity. Advanced semiconductors need smaller efficient chips to function properly which leads directly to the requirement for state-of-the-art lithography equipment to print complex patterns for the newest semiconductor applications. Semiconductor manufacturers need to maintain constant advancements because customers now seek advanced processors and memory modules and integrated circuits within faster multi-functional products that power modern electronics. Consumer electronics chip complexity has grown because of 5G technology and augmented reality (AR) and virtual reality (VR) and artificial intelligence (AI). Chips for next-generation devices need advanced lithographic patterns that EUV lithography tools provide to make these patterns possible. Advanced lithography solutions will maintain a steady market demand because consumer electronics remain a leading force in technological innovation that drives continuous growth of smaller and faster semiconductor devices.

High capital investments – The high capital investments along with operating costs act as major barriers against the market acceptance of lithography equipment that includes advanced technologies such as extreme ultraviolet (EUV) lithography. The total cost for buying and installing lithography machines spans hundreds of millions of dollars at the beginning. Advanced systems need state-of-the-art technology together with exact engineering applications to achieve their costly price point. Advanced semiconductor manufacturers including medium to small-scale organizations may find it difficult to handle the substantial financial costs of equipment acquisition. Stable operation of these systems needs continuous maintenance procedures together with calibration procedures for optimum performance. The implementation of skilled technicians and engineers for operating and equipment maintenance contributes extra to equipment expenses. The machines use abundant power while needing specific materials which cost a lot to acquire. Operating these systems in cleanroom environments creates continued costs for systems that filter air and control temperatures while preventing contamination within the environment. Organizations with budgetary restrictions or practitioners using basic technologies face significant hurdles to acquire advanced lithography tools because of their high installation expenses along with recurrent operational expenses.

Increasing research and development expenditure – The increased demand for semiconductors drives both public and commercial enterprises to construct brand new fabs and enhance their existing facilities. The establishment of these strategic investments serves to enhance manufacturing output as well as maintain current semiconductor technological progress. The strategic need for local semiconductor production has driven governments from the United States and Europe together with Asian countries to provide financial support through incentives with additional funding for building domestic semiconductor facilities. Governments worldwide are investing in semiconductor production due to supply chain needs including EUV lithography technology for making small-scale chips. Private semiconductor and electronics firms increase their R&D expenditures to advance the manufacturing of chips through innovative means. The synergy of public funding support with private industrial investments accelerates the deployment of advanced lithography tools to guarantee semiconductor manufacturing will support emerging technologies as well as global high-tech applications.

The regions analyzed for the market include North America, Europe, South America, Asia Pacific, the Middle East, and Africa. Asia Pacific emerged as the most significant global lithography equipment market, with a 38% market revenue share in 2024.

The Asia-Pacific (APAC) region leads the market for lithography equipment because it operates as the fundamental core of worldwide semiconductor production systems. The APAC region houses the three largest semiconductor manufacturing corporations Taiwan Semiconductor Manufacturing Company (TSMC) Samsung and GlobalFoundries who lead the market demand for advanced lithography systems. Photolithography and extreme ultraviolet (EUV) lithography equipment receives substantial orders from these companies to meet the ever-growing need for microchips which power consumer electronics as well as automotive systems together with emerging technologies such as 5G and AI.

Asia Pacific Region Lithography Equipment Market Share in 2024 - 38%

www.thebrainyinsights.com

Check the geographical analysis of this market by requesting a free sample

The technology segment is divided into photolithography and extreme ultraviolet (EUV) lithography. The photolithography segment dominated the market, with a market share of around 57% in 2024. Photolithography maintains its status as the top technology in lithography equipment markets because it demonstrates reliable functionality while offering scalability together with cost-efficient semiconductor manufacturing processes. Ultraviolet light serves as the principal technology for semiconductor devices manufacturing through photolithography by imprinting complex circuit designs onto semiconductor wafers. Chip production has existed through photolithography technology for multiple decades because it efficiently supports diverse semiconductor node scales and production methods. Photolithography demonstrates outstanding precision by enabling the production of small-sized semiconductor chips. The semiconductor industry can rely on these systems because they function at high production volumes while being established and commercially offered. Photolithography systems provide better value compared to the advanced EUV lithography system due to its higher equipment costs and operational difficulties.

The application segment is divided into semiconductor manufacturing and display manufacturing. The semiconductor manufacturing segment dominated the market, with a market share of around 61% in 2024. Semiconductor manufacturers use lithography technology to create microchip patterns and circuits that power all electronic products including mobile phones and computers as well as automobiles and internet-connected devices. The semiconductor foundries TSMC and Samsung along with Intel buy advanced lithography systems primarily to make high-performance microprocessors and integrated circuits and memory chips. New technologies including artificial intelligence (AI) and 5G connectivity and autonomous vehicles depend on exceptional semiconductor parts for their operation. Market demand for high-precision lithography tools in semiconductor manufacturing will support continuous advancement of the industry due to growing requirements for more powerful and complex chips.

The end use industry segment is divided into semiconductor industry and electronics and automotive industries. The semiconductor industry segment dominated the market, with a market share of around 58% in 2024. Lithography equipment finds its primary market application in semiconductors because these components drive various present-day technological systems. Gas and electronic chips make up basic components across all product categories including consumer gadgets as well as industrial devices and automotive systems and revolutionary technologies including AI systems and IoT infrastructure. The increase in electronic device purchases worldwide leads the semiconductor industry to become the biggest market for lithography equipment. Semiconductor producers including TSMC, Samsung and Intel depend on advanced lithography systems for manufacturing integrated circuits together with memory chips and microprocessors because these companies determine the market demand. The massive scale of the semiconductor industry together with escalating high-performance chip requirements from various sectors gives it primacy in advancing global lithography equipment markets.

| Attribute | Description |

|---|---|

| Market Size | Revenue (USD Billion) |

| Market size value in 2024 | USD 30 Billion |

| Market size value in 2034 | USD 64.76 Billion |

| CAGR (2025 to 2034) | 8% |

| Historical data | 2021-2023 |

| Base Year | 2024 |

| Forecast | 2025-2034 |

| Region | The regions analyzed for the market are Asia Pacific, Europe, South America, North America, and Middle East and Africa. Furthermore, the regions are further analyzed at the country level. |

| Segments | Technology, Application and End Use Industry |

As per The Brainy Insights, the size of the global lithography equipment market was valued at USD 30 billion in 2024 to USD 64.76 billion by 2034.

Global lithography equipment market is growing at a CAGR of 8% during the forecast period 2025-2034.

The market's growth will be influenced by the increasing demand for consumer electronics.

High capital investments could hamper the market growth.

This study forecasts revenue at global, regional, and country levels from 2021 to 2034. The Brainy Insights has segmented the global lithography equipment market based on below mentioned segments:

Global Lithography Equipment Market by Technology:

Global Lithography Equipment Market by Application:

Global Lithography Equipment Market by End Use Industry:

Global Lithography Equipment Market by Region:

Research has its special purpose to undertake marketing efficiently. In this competitive scenario, businesses need information across all industry verticals; the information about customer wants, market demand, competition, industry trends, distribution channels etc. This information needs to be updated regularly because businesses operate in a dynamic environment. Our organization, The Brainy Insights incorporates scientific and systematic research procedures in order to get proper market insights and industry analysis for overall business success. The analysis consists of studying the market from a miniscule level wherein we implement statistical tools which helps us in examining the data with accuracy and precision.

Our research reports feature both; quantitative and qualitative aspects for any market. Qualitative information for any market research process are fundamental because they reveal the customer needs and wants, usage and consumption for any product/service related to a specific industry. This in turn aids the marketers/investors in knowing certain perceptions of the customers. Qualitative research can enlighten about the different product concepts and designs along with unique service offering that in turn, helps define marketing problems and generate opportunities. On the other hand, quantitative research engages with the data collection process through interviews, e-mail interactions, surveys and pilot studies. Quantitative aspects for the market research are useful to validate the hypotheses generated during qualitative research method, explore empirical patterns in the data with the help of statistical tools, and finally make the market estimations.

The Brainy Insights offers comprehensive research and analysis, based on a wide assortment of factual insights gained through interviews with CXOs and global experts and secondary data from reliable sources. Our analysts and industry specialist assume vital roles in building up statistical tools and analysis models, which are used to analyse the data and arrive at accurate insights with exceedingly informative research discoveries. The data provided by our organization have proven precious to a diverse range of companies, facilitating them to address issues such as determining which products/services are the most appealing, whether or not customers use the product in the manner anticipated, the purchasing intentions of the market and many others.

Our research methodology encompasses an idyllic combination of primary and secondary initiatives. Key phases involved in this process are listed below:

The phase involves the gathering and collecting of market data and its related information with the help of different sources & research procedures.

The data procurement stage involves in data gathering and collecting through various data sources.

This stage involves in extensive research. These data sources includes:

Purchased Database: Purchased databases play a crucial role in estimating the market sizes irrespective of the domain. Our purchased database includes:

Primary Research: The Brainy Insights interacts with leading companies and experts of the concerned domain to develop the analyst team’s market understanding and expertise. It improves and substantiates every single data presented in the market reports. Primary research mainly involves in telephonic interviews, E-mail interactions and face-to-face interviews with the raw material providers, manufacturers/producers, distributors, & independent consultants. The interviews that we conduct provides valuable data on market size and industry growth trends prevailing in the market. Our organization also conducts surveys with the various industry experts in order to gain overall insights of the industry/market. For instance, in healthcare industry we conduct surveys with the pharmacists, doctors, surgeons and nurses in order to gain insights and key information of a medical product/device/equipment which the customers are going to usage. Surveys are conducted in the form of questionnaire designed by our own analyst team. Surveys plays an important role in primary research because surveys helps us to identify the key target audiences of the market. Additionally, surveys helps to identify the key target audience engaged with the market. Our survey team conducts the survey by targeting the key audience, thus gaining insights from them. Based on the perspectives of the customers, this information is utilized to formulate market strategies. Moreover, market surveys helps us to understand the current competitive situation of the industry. To be precise, our survey process typically involve with the 360 analysis of the market. This analytical process begins by identifying the prospective customers for a product or service related to the market/industry to obtain data on how a product/service could fit into customers’ lives.

Secondary Research: The secondary data sources includes information published by the on-profit organizations such as World bank, WHO, company fillings, investor presentations, annual reports, national government documents, statistical databases, blogs, articles, white papers and others. From the annual report, we analyse a company’s revenue to understand the key segment and market share of that organization in a particular region. We analyse the company websites and adopt the product mapping technique which is important for deriving the segment revenue. In the product mapping method, we select and categorize the products offered by the companies catering to domain specific market, deduce the product revenue for each of the companies so as to get overall estimation of the market size. We also source data and analyses trends based on information received from supply side and demand side intermediaries in the value chain. The supply side denotes the data gathered from supplier, distributor, wholesaler and the demand side illustrates the data gathered from the end customers for respective market domain.

The supply side for a domain specific market is analysed by:

The demand side for the market is estimated through:

In-house Library: Apart from these third-party sources, we have our in-house library of qualitative and quantitative information. Our in-house database includes market data for various industry and domains. These data are updated on regular basis as per the changing market scenario. Our library includes, historic databases, internal audit reports and archives.

Sometimes there are instances where there is no metadata or raw data available for any domain specific market. For those cases, we use our expertise to forecast and estimate the market size in order to generate comprehensive data sets. Our analyst team adopt a robust research technique in order to produce the estimates:

Data Synthesis: This stage involves the analysis & mapping of all the information obtained from the previous step. It also involves in scrutinizing the data for any discrepancy observed while data gathering related to the market. The data is collected with consideration to the heterogeneity of sources. Robust scientific techniques are in place for synthesizing disparate data sets and provide the essential contextual information that can orient market strategies. The Brainy Insights has extensive experience in data synthesis where the data passes through various stages:

Market Deduction & Formulation: The final stage comprises of assigning data points at appropriate market spaces so as to deduce feasible conclusions. Analyst perspective & subject matter expert based holistic form of market sizing coupled with industry analysis also plays a crucial role in this stage.

This stage involves in finalization of the market size and numbers that we have collected from data integration step. With data interpolation, it is made sure that there is no gap in the market data. Successful trend analysis is done by our analysts using extrapolation techniques, which provide the best possible forecasts for the market.

Data Validation & Market Feedback: Validation is the most important step in the process. Validation & re-validation via an intricately designed process helps us finalize data-points to be used for final calculations.

The Brainy Insights interacts with leading companies and experts of the concerned domain to develop the analyst team’s market understanding and expertise. It improves and substantiates every single data presented in the market reports. The data validation interview and discussion panels are typically composed of the most experienced industry members. The participants include, however, are not limited to:

Moreover, we always validate our data and findings through primary respondents from all the major regions we are working on.

Free Customization

Fortune 500 Clients

Free Yearly Update On Purchase Of Multi/Corporate License

Companies Served Till Date