- +1-315-215-1633

- sales@thebrainyinsights.com

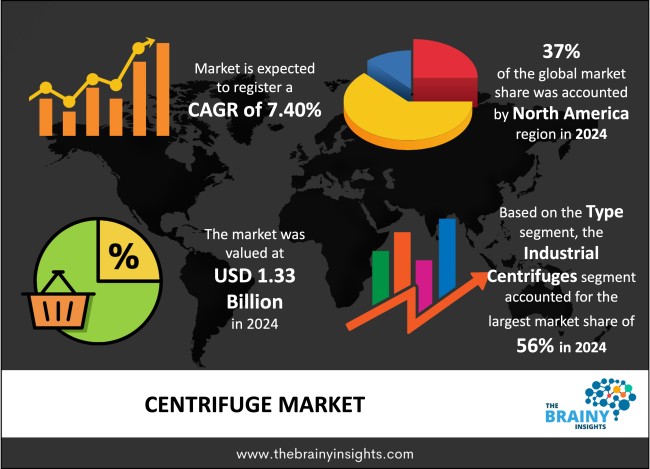

The global centrifuge market was valued at USD 1.33 billion in 2024 and grew at a CAGR of 7.40% from 2025 to 2034. The market is expected to reach USD 2.71 billion by 2034. The increasing demand for diagnostics given the rising incidence and prevalence of chronic and infectious diseases will drive the growth of the global centrifuge market.

Centrifuges operate as mechanical equipment. They apply centrifugal force to split differing density mixtures in a single container. A spinning motion of a container applies centrifugal force which drives denser substances toward the outer wall but leaves lighter substances in the container centre. Laboratories, medical facilities and industrial companies widely implement centrifuges because they facilitate blood-separation, chemical purification tasks and biological sample preparation. High-centrifuges function at very high-speed frequencies with molecular and subcellular separation capabilities and low-speed centrifuges serve predominantly for clinical and industrial applications. Studies often group centrifuges into two categories: fixed-angle rotors which keep the container tubes stationary at one position and swinging-bucket rotors which allow the tubes to shift outwards when spinning to achieve superior separation results. Blood cells and plasma separation during disease diagnosis strongly depends on medical centrifuges. Industrial operations depend heavily on centrifuges to manage wastewater processes and support food manufacturing as well as pharmaceutical production. The technology finds its applications in both nuclear energy sectors and fuel enrichment procedures. The efficiency rating of centrifuges depends on three main factors which are rotational speed and radius combined with the density contrasts between components. The widespread applications of centrifuges across scientific, medical, and industrial fields highlight their importance in modern technology and research.

Get an overview of this study by requesting a free sample

The increasing need for diagnostic capabilities given the rising prevalence of diseases – The healthcare and diagnostics sector demand more centrifuges as chronic and infectious disease prevalence increases. These tools facilitate frequent blood testing, diagnosis and advanced medical research. The increasing global occurrence of cancer together with cardiovascular diseases and infectious outbreaks requires laboratories and hospitals to find efficient blood component separation, plasma extraction and diagnostic sample processing methods which are facilitated by centrifuges. Medical progress in customized treatments and regenerative medicine therapy platforms increases demand for high-speed centrifuges used for the isolation of cells together with proteins and genetic material. Modern healthcare relies heavily on centrifuges because of their essential role in clinical laboratories', point-of-care testing and rapid diagnostic processes. The widespread practice of blood banking combined with research on stem cells is directly boosting the adoption of special centrifuges used for cell preservation and therapeutic purposes. The growing pharmaceutical and biotechnology sectors enhance product demand for centrifuges at an unprecedented rate. Pharmaceutical and biotech organizations extending their R&D operations and production capabilities create an increasing need for modern automated centrifugation systems with enhanced efficiency.

High costs of centrifuges – High acquisition and operating expenses deter many laboratories and research entities especially in the developing nations from adopting centrifuges. Further outlay of capital is required for buying rotors along with adapters and supplementary equipment that increases financial commitment of companies towards these devices. More money needs to be spent on ongoing maintenance services. Laboratories as well as industrial facilities must build specialized infrastructure that includes vibration-free surfaces, temperature controls and stable power supply systems which also increases their operational costs. Complex operational requirements coupled with the necessity of skilled operators also limit the market’s growth. The correct operation of centrifuges particularly high-speed and ultracentrifuges demands specialized expertise from operators which limits the market’s growth. Many regions face a shortage of skilled workers.

Increasing research and development expenditure – Modern centrifuges use improved technology which enhances processing speed while improving accuracy through automated workflows so their usage expands throughout different industrial sectors. The modern version of centrifuges incorporates high-speed operations together with enhanced rotor designs and safety systems that boost efficiency for biological and chemical substance separation. Sample integrity stays intact because of the newly developed refrigerated and vacuum centrifuges which expand their application range into sensitive biomedical and pharmaceutical processes. IoT-connected centrifuges which incorporate artificial intelligence technology transform laboratory management through continuous monitoring and predictive maintenance functionality and automated workflow enhancement. The creation of microfluidic centrifuges has achieved better point-of-care diagnostic as well as research sample processing outcomes by delivering compact energy-efficient devices. The combination of energy-efficient technologies and reduced noises and vibrations in these products delivers superior usability and more sustainable operation to users. Scientific and market demand rises as advanced centrifuge technology establishes cheaper, reliable equipment available across commercial as well as research domains.

The regions analyzed for the market include North America, Europe, South America, Asia Pacific, the Middle East, and Africa. North America emerged as the most significant global centrifuge market, with a 37% market revenue share in 2024.

The North American market dominates the global centrifuge industry because it features well-developed healthcare facilities together with robust pharmaceutical and biotechnology sectors and substantial R&D funding. Leading biotechnology firms together with pharmaceutical giants and advanced diagnostic laboratories operate within this area and they heavily rely on centrifuges to support their drug discovery activities, vaccine production, molecular diagnostics and clinical research initiatives. Due to a high incidence of cancer, cardiovascular diseases and infectious illnesses hospitals; diagnostic laboratories require increasing numbers of diagnostic tests and blood compartment separations thus driving centrifuge market demand. Government support together with private investment into life sciences research of genomics and proteomics has increased the utilization of high-speed and ultracentrifuges in academic research facilities. The advanced healthcare framework along with an outstanding biotech industry and steady technological advances keep North America as the dominant force in the global centrifuge market.

North America Region Centrifuge Market Share in 2024 - 37%

www.thebrainyinsights.com

Check the geographical analysis of this market by requesting a free sample

The type segment is divided into industrial centrifuges and laboratory centrifuges. The industrial centrifuges segment dominated the market, with a market share of around 56% in 2024. Industrial centrifuges offer extensive applications in high-demand sectors such as oil and gas, wastewater treatment, chemical processing, food and beverage and pharmaceutical operations. Manufacturers in the chemical sector and pharmaceutical industry depend heavily on industrial centrifuges to achieve adequate separation of their fine chemicals alongside active pharmaceutical ingredients (APIs) and solvents. The increasing market needs for biopharmaceuticals vaccines and specialty chemicals create additional demand for their adoption.

The design segment is divided into sedimentation centrifuges and filtering centrifuges. The sedimentation centrifuges segment dominated the market, with a market share of around 52% in 2024. Sedimentation centrifuges are used in various sectors including manufacturing sectors, wastewater treatment, chemical processing, pharmaceutical production, food and beverage and oil and gas industries. Sedimentation centrifuges like decanter centrifuges serve numerous applications in water treatment operations for sludge dewatering purposes and solid-liquid separations which help both treatment efficiency and environmental conservation. The chemical and pharmaceutical sectors depend on sedimentation centrifuges for their API purification and fine chemical separation processes. Sedimentation centrifuges enhance the food and beverage industry by defining juice clarity and separating dairy products and extracting pure edible oils which supports consistent product quality and purity. Sustainable industries rely on sedimentation centrifuges to produce biogas and biofuels which boosts their market usefulness. The sedimentation centrifuge stays dominant in the centrifuge market because of its high-capacity efficiency and continuous operation along with its minimal maintenance needs and process flexibility which provides effective and scalable solutions for vital separation needs.

The speed segment is divided into high-speed centrifuges and low-speed centrifuges. The high-speed centrifuges segment dominated the market, with a market share of around 54% in 2024. The operating range for these centrifuges spans from 10000 RPM to more than 100000 RPM thus creating efficient separation of particles down to subcellular scale and proteins while extracting nucleic acids in medical biological and industrial systems. These instruments perform precise and high-purity separations which makes them better than low-speed models on the market. The pharmaceutical and biotechnology industries rely heavily on high-speed centrifuges. The rising market demand for biopharmaceuticals together with monoclonal antibodies and gene therapies has pushed manufacturers to implement these devices more extensively. Academic and research organizations use these centrifuges extensively in DNA/RNA isolation, virus separation processes and cell pelleting procedures for molecular biology experiments to achieve precise experimental findings. The market demand increases because both private organizations and government institutions have stepped up their funding of life sciences research. The performance and user experience of high-speed centrifuges have improved through the integration of automation technology along with digital control systems which also brought improved energy efficiency benefits.

The end-user segment is divided into hospitals & diagnostic laboratories, pharmaceutical & biotechnology companies and industrial & environmental sectors. The hospitals and diagnostic laboratories segment dominated the market, with a share of around 33% in 2024. The market leadership belongs to hospitals and diagnostic laboratories due to rising blood testing requirements. Hospitals perform more surgical procedures and conduct more organ transplants and manage trauma cases and they need continuous blood component supplies which results in increased centrifuge operation. The COVID-19 pandemic elevated the significance of centrifuges during PCR testing and vaccine research thereby leading to broader acceptance within diagnostic laboratories. The operational efficiency of centrifuges has increased due to technological advancements like automated systems and digital interfaces and real-time monitoring features that benefit both hospital workers and laboratory technicians. The market growth for centrifuges persists because hospitals along with diagnostic laboratories continue to use these devices in critical diagnostic applications given the high testing loads and rigorous regulatory standards.

| Attribute | Description |

|---|---|

| Market Size | Revenue (USD Billion) |

| Market size value in 2024 | USD 1.33 Billion |

| Market size value in 2034 | USD 2.71 Billion |

| CAGR (2025 to 2034) | 7.40% |

| Historical data | 2021-2023 |

| Base Year | 2024 |

| Forecast | 2025-2034 |

| Region | The regions analyzed for the market are Asia Pacific, Europe, South America, North America, and Middle East and Africa. Furthermore, the regions are further analyzed at the country level. |

| Segments | Type, Design, Speed and End User |

As per The Brainy Insights, the size of the global centrifuge market was valued at USD 1.33 billion in 2024 to USD 2.71 billion by 2034.

Global centrifuge market is growing at a CAGR of 7.40% during the forecast period 2025-2034.

The market's growth will be influenced by the increasing need for diagnostic capabilities given the rising prevalence of diseases.

High costs of centrifuges could hamper the market growth.

This study forecasts revenue at global, regional, and country levels from 2021 to 2034. The Brainy Insights has segmented the global centrifuge market based on below mentioned segments:

Global Centrifuge Market by Type:

Global Centrifuge Market by Design:

Global Centrifuge Market by Speed:

Global Centrifuge Market by End User:

Global Centrifuge Market by Region:

Research has its special purpose to undertake marketing efficiently. In this competitive scenario, businesses need information across all industry verticals; the information about customer wants, market demand, competition, industry trends, distribution channels etc. This information needs to be updated regularly because businesses operate in a dynamic environment. Our organization, The Brainy Insights incorporates scientific and systematic research procedures in order to get proper market insights and industry analysis for overall business success. The analysis consists of studying the market from a miniscule level wherein we implement statistical tools which helps us in examining the data with accuracy and precision.

Our research reports feature both; quantitative and qualitative aspects for any market. Qualitative information for any market research process are fundamental because they reveal the customer needs and wants, usage and consumption for any product/service related to a specific industry. This in turn aids the marketers/investors in knowing certain perceptions of the customers. Qualitative research can enlighten about the different product concepts and designs along with unique service offering that in turn, helps define marketing problems and generate opportunities. On the other hand, quantitative research engages with the data collection process through interviews, e-mail interactions, surveys and pilot studies. Quantitative aspects for the market research are useful to validate the hypotheses generated during qualitative research method, explore empirical patterns in the data with the help of statistical tools, and finally make the market estimations.

The Brainy Insights offers comprehensive research and analysis, based on a wide assortment of factual insights gained through interviews with CXOs and global experts and secondary data from reliable sources. Our analysts and industry specialist assume vital roles in building up statistical tools and analysis models, which are used to analyse the data and arrive at accurate insights with exceedingly informative research discoveries. The data provided by our organization have proven precious to a diverse range of companies, facilitating them to address issues such as determining which products/services are the most appealing, whether or not customers use the product in the manner anticipated, the purchasing intentions of the market and many others.

Our research methodology encompasses an idyllic combination of primary and secondary initiatives. Key phases involved in this process are listed below:

The phase involves the gathering and collecting of market data and its related information with the help of different sources & research procedures.

The data procurement stage involves in data gathering and collecting through various data sources.

This stage involves in extensive research. These data sources includes:

Purchased Database: Purchased databases play a crucial role in estimating the market sizes irrespective of the domain. Our purchased database includes:

Primary Research: The Brainy Insights interacts with leading companies and experts of the concerned domain to develop the analyst team’s market understanding and expertise. It improves and substantiates every single data presented in the market reports. Primary research mainly involves in telephonic interviews, E-mail interactions and face-to-face interviews with the raw material providers, manufacturers/producers, distributors, & independent consultants. The interviews that we conduct provides valuable data on market size and industry growth trends prevailing in the market. Our organization also conducts surveys with the various industry experts in order to gain overall insights of the industry/market. For instance, in healthcare industry we conduct surveys with the pharmacists, doctors, surgeons and nurses in order to gain insights and key information of a medical product/device/equipment which the customers are going to usage. Surveys are conducted in the form of questionnaire designed by our own analyst team. Surveys plays an important role in primary research because surveys helps us to identify the key target audiences of the market. Additionally, surveys helps to identify the key target audience engaged with the market. Our survey team conducts the survey by targeting the key audience, thus gaining insights from them. Based on the perspectives of the customers, this information is utilized to formulate market strategies. Moreover, market surveys helps us to understand the current competitive situation of the industry. To be precise, our survey process typically involve with the 360 analysis of the market. This analytical process begins by identifying the prospective customers for a product or service related to the market/industry to obtain data on how a product/service could fit into customers’ lives.

Secondary Research: The secondary data sources includes information published by the on-profit organizations such as World bank, WHO, company fillings, investor presentations, annual reports, national government documents, statistical databases, blogs, articles, white papers and others. From the annual report, we analyse a company’s revenue to understand the key segment and market share of that organization in a particular region. We analyse the company websites and adopt the product mapping technique which is important for deriving the segment revenue. In the product mapping method, we select and categorize the products offered by the companies catering to domain specific market, deduce the product revenue for each of the companies so as to get overall estimation of the market size. We also source data and analyses trends based on information received from supply side and demand side intermediaries in the value chain. The supply side denotes the data gathered from supplier, distributor, wholesaler and the demand side illustrates the data gathered from the end customers for respective market domain.

The supply side for a domain specific market is analysed by:

The demand side for the market is estimated through:

In-house Library: Apart from these third-party sources, we have our in-house library of qualitative and quantitative information. Our in-house database includes market data for various industry and domains. These data are updated on regular basis as per the changing market scenario. Our library includes, historic databases, internal audit reports and archives.

Sometimes there are instances where there is no metadata or raw data available for any domain specific market. For those cases, we use our expertise to forecast and estimate the market size in order to generate comprehensive data sets. Our analyst team adopt a robust research technique in order to produce the estimates:

Data Synthesis: This stage involves the analysis & mapping of all the information obtained from the previous step. It also involves in scrutinizing the data for any discrepancy observed while data gathering related to the market. The data is collected with consideration to the heterogeneity of sources. Robust scientific techniques are in place for synthesizing disparate data sets and provide the essential contextual information that can orient market strategies. The Brainy Insights has extensive experience in data synthesis where the data passes through various stages:

Market Deduction & Formulation: The final stage comprises of assigning data points at appropriate market spaces so as to deduce feasible conclusions. Analyst perspective & subject matter expert based holistic form of market sizing coupled with industry analysis also plays a crucial role in this stage.

This stage involves in finalization of the market size and numbers that we have collected from data integration step. With data interpolation, it is made sure that there is no gap in the market data. Successful trend analysis is done by our analysts using extrapolation techniques, which provide the best possible forecasts for the market.

Data Validation & Market Feedback: Validation is the most important step in the process. Validation & re-validation via an intricately designed process helps us finalize data-points to be used for final calculations.

The Brainy Insights interacts with leading companies and experts of the concerned domain to develop the analyst team’s market understanding and expertise. It improves and substantiates every single data presented in the market reports. The data validation interview and discussion panels are typically composed of the most experienced industry members. The participants include, however, are not limited to:

Moreover, we always validate our data and findings through primary respondents from all the major regions we are working on.

Free Customization

Fortune 500 Clients

Free Yearly Update On Purchase Of Multi/Corporate License

Companies Served Till Date