- +1-315-215-1633

- sales@thebrainyinsights.com

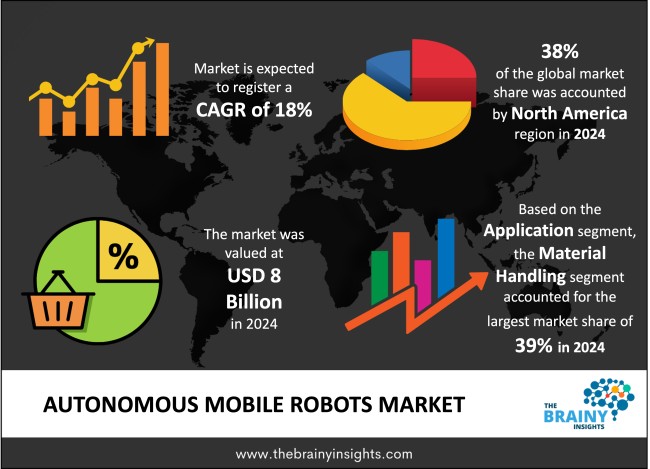

The global autonomous mobile robots market was valued at USD 8 billion in 2024 and grew at a CAGR of 18% from 2025 to 2034. The market is expected to reach USD 41.87 billion by 2034. The trend of industrial automation 4.0 will drive the growth of the global autonomous mobile robots market.

Intelligent self-operating autonomous systems named Autonomous Mobile Robots (AMRs) complete their missions independently of human operator intervention by making sense of their environment. The robotic devices use sensors coupled with cameras and elaborate algorithms to understand their surroundings. Autonomous Mobile Robots feature LiDAR alongside radar and ultrasonic sensors and vision systems, enabling them to generate environmental maps and execute instant decision-making processes. The main distinction between AMRs and Automated Guided Vehicles (AGVs) is the absence of track-like movements from AMRs, which allows for more flexible task performance in any direction. AMRs function through core enabling technologies incorporating artificial intelligence (AI), machine learning and computer vision to become adaptable in unpredictable surroundings. Robotics solutions operate across warehouses, factories, hospitals, and public environments to handle materials and deliver items, permitting space surveillance tasks. Humans can concentrate on crucial or strategic work through robotic automation because AMRs execute systematic tasks. An autonomous operational system leads to improved overall efficiency, increased productivity, and enhanced safety features through reduced potential errors in dangerous areas. AMRs establish environmental maps by employing simultaneous localization and mapping (SLAM) procedures, which initialize and update these positional frameworks. The scalable nature of AMRs and their ability to adapt represents the main benefit of these robotic systems. These robots work in multiple business environments, including e-commerce with logistics services and healthcare facilities, and receive programming instructions for various operational tasks.

Get an overview of this study by requesting a free sample

The trend of Industrialization 4.0 – The industrial automation trend has emerged as a major factor that drives companies to adopt Autonomous Mobile Robots (AMRs). Businesses throughout different sectors attempt operational efficiency improvements through autonomous mobile robots because these systems can streamline manual and repetitious activities, including material movement operations, inventory control functions, and delivery tasks. Implementing autonomous mobile robots in logistics manufacturing and e-commerce sectors leads to automated critical process operations that require fewer human employees and provide error-prevention benefits. Rapid and dependable production schedules and extended delivery timelines continue to drive industries toward automation adoption. Research advancements have transformed automated mobile robots from mere scientific devices to flexible industrial tools that industries can now easily utilise. Technological advances have extended the capacities of AMRs regarding what tasks they can perform, transforming them into critical operational assets in automation and flexibility-reliant areas such as healthcare, manufacturing, and logistics.

High initial investment costs of autonomous mobile robots – The high initial investment required to acquire Autonomous Mobile Robots (AMRs) creates the biggest challenge in their adoption. Implementing Autonomous Mobile Robots and their corresponding purchase costs substantially strains financial resources that mostly burden smaller and medium-sized businesses (SMEs). High initial expenses stem from advanced sensing components, artificial intelligence implementation, and necessary infrastructure changes. Executing AMR implementation demands additional costs for employee training as well. Volatile capital expenditure limits many businesses from implementing AMRs despite the robotic systems' long-term advantages of higher operational efficiency, labour reduction and security improvements. Technological limitations also pose significant challenges for AMR adoption. Current AMR technology demonstrates improved capabilities but struggles to navigate complex, dynamic warehouse environments. When working in crowded or condensed environments, AMRs demonstrate difficulty operating effectively because they experience trouble seeing obstacles or managing delicate objects that are poorly shaped.

The growth of retail and e-commerce – E-commerce sales growth in fields including food delivery and electronics drives warehouses to function at absolute peak speeds. At the same time, the fashion industry also requires improved responsiveness. AMRs resolve these requirements by robotically executing fundamental processes such as order selection, item arrangement, and physical delivery operations in streamlined distribution facilities. Through automated operations and enhanced performance, AMRs help suppliers fulfil customer needs by meeting critical timeframes and decreasing human mistakes, leading to better end-user satisfaction. A key benefit of scalable automated mobile robots (AMRs) is their ability to help companies handle changing demand levels through flexible operational adjustments across peak shopping periods. Implementing AMRs into e-commerce logistics systems delivers enhanced operational efficiency and increased throughput capability while reducing personnel expenses, which is crucial for businesses to maintain slim profitability.

The regions analyzed for the market include North America, Europe, South America, Asia Pacific, the Middle East, and Africa. North America emerged as the most significant global autonomous mobile robots market, with a 38% market revenue share in 2024.

Advancements in robotics, AI, and automation technologies throughout the region enable the progressive development and implementation of Autonomous Mobile Robots. E-commerce growth is a primary driver for AMR adoption because companies use these autonomous robots to improve warehouse operations. AMR adoption is prominent in manufacturing alongside industrial applications, including automotive manufacturing, aerospace production and electronics production, where companies utilize AMRs to optimize their manufacturing operations. Major AMR producers Amazon Robotics, Fetch Robotics, and KUKA Robotics established North America as a technology pioneer in the global AMR market. The market grows stronger because governments promote automation adoption by providing benefits and welcoming policy frameworks across various industries.

North America Region Autonomous Mobile Robots Market Share in 2024 - 38%

www.thebrainyinsights.com

Check the geographical analysis of this market by requesting a free sample

The application segment is divided into material handling, security and surveillance and delivery and logistics. The material handling segment dominated the market, with a market share of around 39% in 2024. Automated material handling remains the foremost application for Autonomous Mobile Robots (AMRs) because industrial environments leverage these machines to accomplish efficient material movements with maximum precision while decreasing operational costs. Daily operational requirements within logistics, manufacturing, and warehousing depend heavily on goods and materials transportation in their sectors. The automated system decreases workforce dependency while reducing risks and speeding up process execution. The growing e-commerce industry pushes warehouse and distribution facilities to rapidly process increased product volumes by adopting Autonomous Mobile Robots for material handling work. Combining AMRs with existing warehouse management systems (WMS) creates stronger operational effectiveness while increasing system scalability. The growth of AI alongside machine learning and sensor technologies has improved autonomous mobile robots while making them less expensive and more dependable, which has increased their popularity. The material-handling automation segment will exhibit prominent demand for AMRs throughout the upcoming years because businesses need these systems to maintain competitiveness while minimizing operational expenses.

The end-user industry segment is divided into logistics and warehousing, automotive, healthcare and retail. The logistics and warehousing segment dominated the market, with a market share of around 42% in 2024. The Autonomous Mobile Robots (AMRs) market shows the logistics and warehousing sector as its primary end-user segment because of rising supply chain operational automation needs. Rising e-commerce growth demands rapid improvement in logistics and warehousing operations to meet expanding requirements for speedier deliveries alongside enhanced accuracy and operational efficiency standards. These sectors benefit from AMR capabilities, which automate order completion and inventory processing, distribute materials and perform sorting functions. Implementing AMRs results in lower work expenses, fewer mistakes, higher operational output, and maximize operational efficiency. AMRs deliver powerful benefits to large warehouse operations, executing workload operations spanning storage-to-storage movements and product handling, assembly, and inventory replenishment tasks. The robotic machines enable continuous operation while maximizing manufacturing speed to meet urgent delivery needs. Through their compatibility with warehouse management systems (WMS) and cloud-based platforms, AMRs enable workflow optimization, delivering real-time data for enhanced business decisions. The future market demand for automated mobile robots in warehousing and distribution will expand due to rising customer needs for improved delivery speed, lower costs, and higher accuracy, which will strengthen their position within this segment.

The component segment is divided into hardware and software. The hardware segment dominated the market, with a market share of around 60% in 2024. The hardware segment dominates the Autonomous Mobile Robots (AMRs) market since these components create the essential infrastructure that enables AMRs to be effective. Automated mobile robots depend heavily on basic hardware components like sensors, motors, batteries and cameras to navigate autonomously around their environment while executing assigned tasks. Robot autonomy depends heavily on sensors, including LiDAR and ultrasonic sensors alongside cameras, which play a vital role in detecting obstacles and enabling navigation mapping operations. The motion capabilities of AMRs result from motors and actuators, but cameras and other visual sensors enable robots to assess visual data necessary for their picking and sorting duties. Because autonomous robot performance depends strongly on hardware elements, they maintain their position as market leaders in the AMR domain. The growth of the hardware segment owes to enhanced battery performance and energy efficiency, which allows AMRs to sustain operation between charging cycles.

The navigation technology segment is divided into LiDAR, vision-based navigation and magnetic/infrared sensors. The LiDAR segment dominated the market, with a market share of around 37% in 2024. The Autonomous Mobile Robots market depends on LiDAR (Light Detection and Ranging) technology as the key navigation component because it delivers precise maps and dependable performance alongside detailed 3D environmental information. The laser pulse operations of LiDAR systems generate precise 3D map data necessary for AMRs to locate themselves safely through complicated surroundings and spot obstacles without accidents. AMRs excel in adapting to dynamic and cluttered spaces, including outdoor areas, warehouses and factories, because LiDAR technology ensures successful real-time navigation. LiDAR has become the major navigation technology in AMRs because its performance delivers enhanced results beyond visual-based systems or infrared sensors. Through continuous scanning and real-time operating capabilities, LiDAR enables AMRs to make immediate decisions, which results in improved autonomous function and operational effectiveness.

| Attribute | Description |

|---|---|

| Market Size | Revenue (USD Billion) |

| Market size value in 2024 | USD 8 Billion |

| Market size value in 2034 | USD 41.87 Billion |

| CAGR (2025 to 2034) | 18% |

| Historical data | 2021-2023 |

| Base Year | 2024 |

| Forecast | 2025-2034 |

| Region | The regions analyzed for the market are Asia Pacific, Europe, South America, North America, and Middle East and Africa. Furthermore, the regions are further analyzed at the country level. |

| Segments | Application, End User Industry, Component and Navigation Technology |

As per The Brainy Insights, the size of the global autonomous mobile robots market was valued at USD 8 billion in 2024 to USD 41.87 billion by 2034.

Global autonomous mobile robots market is growing at a CAGR of 18% during the forecast period 2025-2034.

The market's growth will be influenced by the trend of industrialization 4.0.

High initial investment costs of autonomous mobile robots could hamper the market growth.

This study forecasts revenue at global, regional, and country levels from 2021 to 2034. The Brainy Insights has segmented the global autonomous mobile robots market based on below mentioned segments:

Global Autonomous Mobile Robots Market by Application:

Global Autonomous Mobile Robots Market by End User Industry:

Global Autonomous Mobile Robots Market by Component:

Global Autonomous Mobile Robots Market by Navigation Technology:

Global Autonomous Mobile Robots Market by Region:

Research has its special purpose to undertake marketing efficiently. In this competitive scenario, businesses need information across all industry verticals; the information about customer wants, market demand, competition, industry trends, distribution channels etc. This information needs to be updated regularly because businesses operate in a dynamic environment. Our organization, The Brainy Insights incorporates scientific and systematic research procedures in order to get proper market insights and industry analysis for overall business success. The analysis consists of studying the market from a miniscule level wherein we implement statistical tools which helps us in examining the data with accuracy and precision.

Our research reports feature both; quantitative and qualitative aspects for any market. Qualitative information for any market research process are fundamental because they reveal the customer needs and wants, usage and consumption for any product/service related to a specific industry. This in turn aids the marketers/investors in knowing certain perceptions of the customers. Qualitative research can enlighten about the different product concepts and designs along with unique service offering that in turn, helps define marketing problems and generate opportunities. On the other hand, quantitative research engages with the data collection process through interviews, e-mail interactions, surveys and pilot studies. Quantitative aspects for the market research are useful to validate the hypotheses generated during qualitative research method, explore empirical patterns in the data with the help of statistical tools, and finally make the market estimations.

The Brainy Insights offers comprehensive research and analysis, based on a wide assortment of factual insights gained through interviews with CXOs and global experts and secondary data from reliable sources. Our analysts and industry specialist assume vital roles in building up statistical tools and analysis models, which are used to analyse the data and arrive at accurate insights with exceedingly informative research discoveries. The data provided by our organization have proven precious to a diverse range of companies, facilitating them to address issues such as determining which products/services are the most appealing, whether or not customers use the product in the manner anticipated, the purchasing intentions of the market and many others.

Our research methodology encompasses an idyllic combination of primary and secondary initiatives. Key phases involved in this process are listed below:

The phase involves the gathering and collecting of market data and its related information with the help of different sources & research procedures.

The data procurement stage involves in data gathering and collecting through various data sources.

This stage involves in extensive research. These data sources includes:

Purchased Database: Purchased databases play a crucial role in estimating the market sizes irrespective of the domain. Our purchased database includes:

Primary Research: The Brainy Insights interacts with leading companies and experts of the concerned domain to develop the analyst team’s market understanding and expertise. It improves and substantiates every single data presented in the market reports. Primary research mainly involves in telephonic interviews, E-mail interactions and face-to-face interviews with the raw material providers, manufacturers/producers, distributors, & independent consultants. The interviews that we conduct provides valuable data on market size and industry growth trends prevailing in the market. Our organization also conducts surveys with the various industry experts in order to gain overall insights of the industry/market. For instance, in healthcare industry we conduct surveys with the pharmacists, doctors, surgeons and nurses in order to gain insights and key information of a medical product/device/equipment which the customers are going to usage. Surveys are conducted in the form of questionnaire designed by our own analyst team. Surveys plays an important role in primary research because surveys helps us to identify the key target audiences of the market. Additionally, surveys helps to identify the key target audience engaged with the market. Our survey team conducts the survey by targeting the key audience, thus gaining insights from them. Based on the perspectives of the customers, this information is utilized to formulate market strategies. Moreover, market surveys helps us to understand the current competitive situation of the industry. To be precise, our survey process typically involve with the 360 analysis of the market. This analytical process begins by identifying the prospective customers for a product or service related to the market/industry to obtain data on how a product/service could fit into customers’ lives.

Secondary Research: The secondary data sources includes information published by the on-profit organizations such as World bank, WHO, company fillings, investor presentations, annual reports, national government documents, statistical databases, blogs, articles, white papers and others. From the annual report, we analyse a company’s revenue to understand the key segment and market share of that organization in a particular region. We analyse the company websites and adopt the product mapping technique which is important for deriving the segment revenue. In the product mapping method, we select and categorize the products offered by the companies catering to domain specific market, deduce the product revenue for each of the companies so as to get overall estimation of the market size. We also source data and analyses trends based on information received from supply side and demand side intermediaries in the value chain. The supply side denotes the data gathered from supplier, distributor, wholesaler and the demand side illustrates the data gathered from the end customers for respective market domain.

The supply side for a domain specific market is analysed by:

The demand side for the market is estimated through:

In-house Library: Apart from these third-party sources, we have our in-house library of qualitative and quantitative information. Our in-house database includes market data for various industry and domains. These data are updated on regular basis as per the changing market scenario. Our library includes, historic databases, internal audit reports and archives.

Sometimes there are instances where there is no metadata or raw data available for any domain specific market. For those cases, we use our expertise to forecast and estimate the market size in order to generate comprehensive data sets. Our analyst team adopt a robust research technique in order to produce the estimates:

Data Synthesis: This stage involves the analysis & mapping of all the information obtained from the previous step. It also involves in scrutinizing the data for any discrepancy observed while data gathering related to the market. The data is collected with consideration to the heterogeneity of sources. Robust scientific techniques are in place for synthesizing disparate data sets and provide the essential contextual information that can orient market strategies. The Brainy Insights has extensive experience in data synthesis where the data passes through various stages:

Market Deduction & Formulation: The final stage comprises of assigning data points at appropriate market spaces so as to deduce feasible conclusions. Analyst perspective & subject matter expert based holistic form of market sizing coupled with industry analysis also plays a crucial role in this stage.

This stage involves in finalization of the market size and numbers that we have collected from data integration step. With data interpolation, it is made sure that there is no gap in the market data. Successful trend analysis is done by our analysts using extrapolation techniques, which provide the best possible forecasts for the market.

Data Validation & Market Feedback: Validation is the most important step in the process. Validation & re-validation via an intricately designed process helps us finalize data-points to be used for final calculations.

The Brainy Insights interacts with leading companies and experts of the concerned domain to develop the analyst team’s market understanding and expertise. It improves and substantiates every single data presented in the market reports. The data validation interview and discussion panels are typically composed of the most experienced industry members. The participants include, however, are not limited to:

Moreover, we always validate our data and findings through primary respondents from all the major regions we are working on.

Free Customization

Fortune 500 Clients

Free Yearly Update On Purchase Of Multi/Corporate License

Companies Served Till Date