- +1-315-215-1633

- sales@thebrainyinsights.com

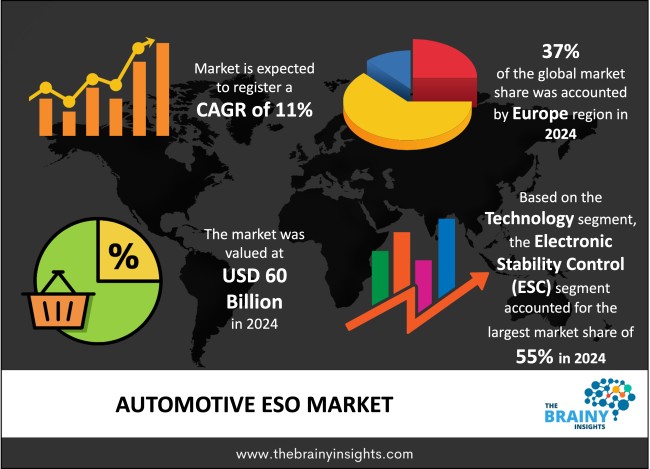

The global automotive ESO market was valued at USD 60 billion in 2024 and grew at a CAGR of 11% from 2025 to 2034. The market is expected to reach USD 170.36 billion by 2034. The stringent regulatory requirements will drive the growth of the global automotive ESO market.

Automotive ESO (Electronic Stability Optimization) comprises advanced technological mobility systems which optimize vehicle stability and safety performance in vital driving scenarios. The continuous monitoring of data points, including speed and steering within vehicles by ESO systems, enables detecting impermissible vehicle handling. When the system detects instability, it activates brakes, power, and steering adjustments to help drivers maintain control while preventing crashes. The automotive ESO's fundamental components comprise sensors and control modules that merge within a vehicle's electronic control unit (ECU). The real-time data acquisition includes wheel slip measurements together with vehicle rotation measurements. Exterior data from the sensors moves across the ECU platform, and the system checks it against established stability guidelines. The system activates target interventions whenever it senses loss of directional control through understeer or oversteer behaviour. ESA has found its prominent application through Electronic Stability Control (ESC), establishing itself as a mandatory system for new vehicles throughout multiple countries over recent years. Some ESO systems integrate advanced driver-assistance systems (ADAS) with traction control, anti-lock braking systems (ABS), and adaptive cruise control. Vehicle stability optimization occurs through systematic operations between these systems, providing security and smoothness during driving conditions. Advanced automotive technology evolution is expected to introduce machine learning algorithms into ESO platforms, enabling the system to react better to diverse driving conditions and boost predictive safety capabilities.

Get an overview of this study by requesting a free sample

Stringent regulatory requirements – The need for automotive Electronic Stability Optimization (ESO) systems, particularly Electronic Stability Control (ESC), arises substantially due to regulatory requirements. Various regions and nations enforce stringent vehicle regulations that require electronic stability control in new vehicles, affecting the automotive market directly. Under the General Safety Regulation (GSR) of the European Union, all new passenger cars and light commercial vehicles must include ESC systems to enhance safety and prevent accidents. The safety regulation enforced ESC implementation on new model vehicles in 2014 and newly registered vehicles starting in 2015. The United States National Highway Traffic Safety Administration required standard ESC installation on all passenger vehicles and light trucks beginning in 2012. Safety organizations established these laws because ESC technology effectively minimizes controlled accident rates, which become substantial in dangerous road conditions. Automakers actively integrate advanced Electronic Stability Systems to meet stricter regulatory requirements and evade penalties from compliance enforcement. Legal requirements for standard compliance have led manufacturers to prioritize ESO systems, making them essential vehicle components driving their global growth.

The high costs of automotive ESO – The development and production of complete Electronic Stability Control (ESC) systems require substantial costs, mainly from manufacturing essential components. These systems need specialized sensors such as accelerometers, gyroscopes, and wheel-speed sensors to track vehicle behaviour in real time. The processing of sensor data by control modules, which activates wheel-specific brake activation, adds additional expense to the overall cost structure. Integrated sensors and control systems increase automobile production expenses; thus, consumers in price-sensitive segments pay higher prices. Manufacturers must spend money on research and development (R&D) alongside testing and regulatory compliance metrics. Advanced software development for stability control throughout driving scenarios requires trained professionals and expensive infrastructure. Research and development expenses, coupled with the system integration effort required for ADAS functionality, significantly increase the costs, which hampers the market's growth.

Rising public awareness – A growing public awareness about safety combined with consumer demand specifically drives the adoption of Automotive Electronic Stability Optimization Systems. Consumers across North American and European markets show rising commitment toward vehicle safety alongside their adoption of advanced driver assistance systems (ADAS) to enhance total driving security. Furthermore, vehicle manufacturers build ESO systems into standard or optional specifications across all price ranges. Safety ratings from Euro NCAP and NHTSA and their crash-test evaluations have encouraged consumers to demand vehicles with accompanying advanced safety technologies including Electronic Stability Control (ESO). Positive safety ratings influence consumer car marketplace choices while forcing automakers to improve stability technology systems for better safety performance.

The regions analyzed for the market include North America, Europe, South America, Asia Pacific, the Middle East, and Africa. Europe emerged as the most significant global automotive ESO market, with a 37% market revenue share in 2024.

The automotive Electronic Stability Optimization (ESO) market shows the highest dominance within Europe because of legislative standards, safety priorities, and manufacturer concentration. ESC technology became mandatory in all new passenger and light commercial vehicles throughout the European Union according to the General Safety Regulation before 2014, which established worldwide standards for safety technologies. Road safety is a priority throughout Europe because organizations like Euro NCAP have established rigorous vehicle safety criteria. ESC is essential in attaining these safety evaluations, so European vehicle buyers actively choose vehicles boasting safety features more frequently. Consumer demand is rising, and demand for ESO systems throughout the region is increasing.

Europe Region Automotive ESO Market Share in 2024 - 37%

www.thebrainyinsights.com

Check the geographical analysis of this market by requesting a free sample

The technology segment is divided into electronic stability control (ESC), traction control system (TCS) and roll-over mitigation. The electronic stability control (ESC) segment dominated the market, with a share of around 55% in 2024. Electronic Stability Control (ESC) maintains its position as market leader for automotive Electronic Stability Optimization (ESO) because of the extensive evidence showing its ability to strengthen vehicle safety and stability. ESC systems use technology to stop skidding and maintain vehicle control during critical driving situations when vehicles understeer or oversteer in dangerous or unfriendly road conditions. Regulatory globalization patterns have supported ESC adoption because dozens of countries now require this technology as a standard feature for new passenger vehicles. The stringent regulatory requirements have expedited vehicle manufacturers to integrate this technology into most passenger car segments. The widespread adoption of ESC has multiplied because detailed safety tests and accident statistics show that ESC effectively lowers fatal accident risks. Combining product integration and increasing consumer need for advanced safety technology makes ESC the market-leading component in automotive ESO systems.

The vehicle type segment is divided into passenger cars, commercial vehicles and electric vehicles (EVs). The passenger cars segment dominated the market, with a market share of around 58% in 2024. Passenger cars now have Electronic Stability Control (ESC) as a basic requirement throughout North America, Europe and Asia due to ESC's statutory presence in new vehicle manufacturing regulations. Production compliance with safety standards under regulatory mandates drives manufacturers to adopt ESO technologies in their passenger vehicles because these technologies help prevent road accidents comprising loss of control. ESO market leadership by passenger vehicles emerges from consumer demand for these advanced safety system features. The passenger cars segment receives the most vehicle sales compared to commercial and electric vehicles (EVs), thus driving broad adoption of ESO systems. The rising global market for passenger cars, primarily in developing economies, will continue to strengthen the segment's dominance in the future.

The application segment is divided into on-road application and off-road application. The on-road application segment dominated the market, with a market share of around 67% in 2024. Vehicles operating in on-road situations encounter numerous challenges to stability from highway to urban street conditions because of surface types, weather variations and movement patterns among other road users. ESC systems protect drivers from accidents created by skidding and understeering or oversteering conditions in adverse weather situations, including snow, rain and ice. On-road applications control the market for ECO because vehicles primarily operate along roads in the global transportation system. All consumers spend their driving time on public roads for daily travel and trips throughout the nation, as well as urban navigation. ESO system adoption keeps growing because governmental requirements for ESC systems exist to protect road safety, especially during passenger vehicle usage. Road safety remains a top priority in North America, Europe, and Asia, and it drives intense regulatory influence, resulting in mandatory ESC requirements for vehicles.

| Attribute | Description |

|---|---|

| Market Size | Revenue (USD Billion) |

| Market size value in 2024 | USD 60 Billion |

| Market size value in 2034 | USD 170.36 Billion |

| CAGR (2025 to 2034) | 11% |

| Historical data | 2021-2023 |

| Base Year | 2024 |

| Forecast | 2025-2034 |

| Region | The regions analyzed for the market are Asia Pacific, Europe, South America, North America, and Middle East and Africa. Furthermore, the regions are further analyzed at the country level. |

| Segments | Technology, Vehicle Type and Application |

As per The Brainy Insights, the size of the global automotive ESO market was valued at USD 60 billion in 2024 to USD 170.36 billion by 2034.

Global automotive ESO market is growing at a CAGR of 11% during the forecast period 2025-2034.

The market's growth will be influenced by stringent regulatory requirements.

The high costs of automotive ESO could hamper the market growth.

This study forecasts revenue at global, regional, and country levels from 2021 to 2034. The Brainy Insights has segmented the global automotive ESO market based on below mentioned segments:

Global Automotive ESO Market by Technology:

Global Automotive ESO Market by Vehicle Type:

Global Automotive ESO Market by Application:

Global Automotive ESO Market by Region:

Research has its special purpose to undertake marketing efficiently. In this competitive scenario, businesses need information across all industry verticals; the information about customer wants, market demand, competition, industry trends, distribution channels etc. This information needs to be updated regularly because businesses operate in a dynamic environment. Our organization, The Brainy Insights incorporates scientific and systematic research procedures in order to get proper market insights and industry analysis for overall business success. The analysis consists of studying the market from a miniscule level wherein we implement statistical tools which helps us in examining the data with accuracy and precision.

Our research reports feature both; quantitative and qualitative aspects for any market. Qualitative information for any market research process are fundamental because they reveal the customer needs and wants, usage and consumption for any product/service related to a specific industry. This in turn aids the marketers/investors in knowing certain perceptions of the customers. Qualitative research can enlighten about the different product concepts and designs along with unique service offering that in turn, helps define marketing problems and generate opportunities. On the other hand, quantitative research engages with the data collection process through interviews, e-mail interactions, surveys and pilot studies. Quantitative aspects for the market research are useful to validate the hypotheses generated during qualitative research method, explore empirical patterns in the data with the help of statistical tools, and finally make the market estimations.

The Brainy Insights offers comprehensive research and analysis, based on a wide assortment of factual insights gained through interviews with CXOs and global experts and secondary data from reliable sources. Our analysts and industry specialist assume vital roles in building up statistical tools and analysis models, which are used to analyse the data and arrive at accurate insights with exceedingly informative research discoveries. The data provided by our organization have proven precious to a diverse range of companies, facilitating them to address issues such as determining which products/services are the most appealing, whether or not customers use the product in the manner anticipated, the purchasing intentions of the market and many others.

Our research methodology encompasses an idyllic combination of primary and secondary initiatives. Key phases involved in this process are listed below:

The phase involves the gathering and collecting of market data and its related information with the help of different sources & research procedures.

The data procurement stage involves in data gathering and collecting through various data sources.

This stage involves in extensive research. These data sources includes:

Purchased Database: Purchased databases play a crucial role in estimating the market sizes irrespective of the domain. Our purchased database includes:

Primary Research: The Brainy Insights interacts with leading companies and experts of the concerned domain to develop the analyst team’s market understanding and expertise. It improves and substantiates every single data presented in the market reports. Primary research mainly involves in telephonic interviews, E-mail interactions and face-to-face interviews with the raw material providers, manufacturers/producers, distributors, & independent consultants. The interviews that we conduct provides valuable data on market size and industry growth trends prevailing in the market. Our organization also conducts surveys with the various industry experts in order to gain overall insights of the industry/market. For instance, in healthcare industry we conduct surveys with the pharmacists, doctors, surgeons and nurses in order to gain insights and key information of a medical product/device/equipment which the customers are going to usage. Surveys are conducted in the form of questionnaire designed by our own analyst team. Surveys plays an important role in primary research because surveys helps us to identify the key target audiences of the market. Additionally, surveys helps to identify the key target audience engaged with the market. Our survey team conducts the survey by targeting the key audience, thus gaining insights from them. Based on the perspectives of the customers, this information is utilized to formulate market strategies. Moreover, market surveys helps us to understand the current competitive situation of the industry. To be precise, our survey process typically involve with the 360 analysis of the market. This analytical process begins by identifying the prospective customers for a product or service related to the market/industry to obtain data on how a product/service could fit into customers’ lives.

Secondary Research: The secondary data sources includes information published by the on-profit organizations such as World bank, WHO, company fillings, investor presentations, annual reports, national government documents, statistical databases, blogs, articles, white papers and others. From the annual report, we analyse a company’s revenue to understand the key segment and market share of that organization in a particular region. We analyse the company websites and adopt the product mapping technique which is important for deriving the segment revenue. In the product mapping method, we select and categorize the products offered by the companies catering to domain specific market, deduce the product revenue for each of the companies so as to get overall estimation of the market size. We also source data and analyses trends based on information received from supply side and demand side intermediaries in the value chain. The supply side denotes the data gathered from supplier, distributor, wholesaler and the demand side illustrates the data gathered from the end customers for respective market domain.

The supply side for a domain specific market is analysed by:

The demand side for the market is estimated through:

In-house Library: Apart from these third-party sources, we have our in-house library of qualitative and quantitative information. Our in-house database includes market data for various industry and domains. These data are updated on regular basis as per the changing market scenario. Our library includes, historic databases, internal audit reports and archives.

Sometimes there are instances where there is no metadata or raw data available for any domain specific market. For those cases, we use our expertise to forecast and estimate the market size in order to generate comprehensive data sets. Our analyst team adopt a robust research technique in order to produce the estimates:

Data Synthesis: This stage involves the analysis & mapping of all the information obtained from the previous step. It also involves in scrutinizing the data for any discrepancy observed while data gathering related to the market. The data is collected with consideration to the heterogeneity of sources. Robust scientific techniques are in place for synthesizing disparate data sets and provide the essential contextual information that can orient market strategies. The Brainy Insights has extensive experience in data synthesis where the data passes through various stages:

Market Deduction & Formulation: The final stage comprises of assigning data points at appropriate market spaces so as to deduce feasible conclusions. Analyst perspective & subject matter expert based holistic form of market sizing coupled with industry analysis also plays a crucial role in this stage.

This stage involves in finalization of the market size and numbers that we have collected from data integration step. With data interpolation, it is made sure that there is no gap in the market data. Successful trend analysis is done by our analysts using extrapolation techniques, which provide the best possible forecasts for the market.

Data Validation & Market Feedback: Validation is the most important step in the process. Validation & re-validation via an intricately designed process helps us finalize data-points to be used for final calculations.

The Brainy Insights interacts with leading companies and experts of the concerned domain to develop the analyst team’s market understanding and expertise. It improves and substantiates every single data presented in the market reports. The data validation interview and discussion panels are typically composed of the most experienced industry members. The participants include, however, are not limited to:

Moreover, we always validate our data and findings through primary respondents from all the major regions we are working on.

Free Customization

Fortune 500 Clients

Free Yearly Update On Purchase Of Multi/Corporate License

Companies Served Till Date