- +1-315-215-1633

- sales@thebrainyinsights.com

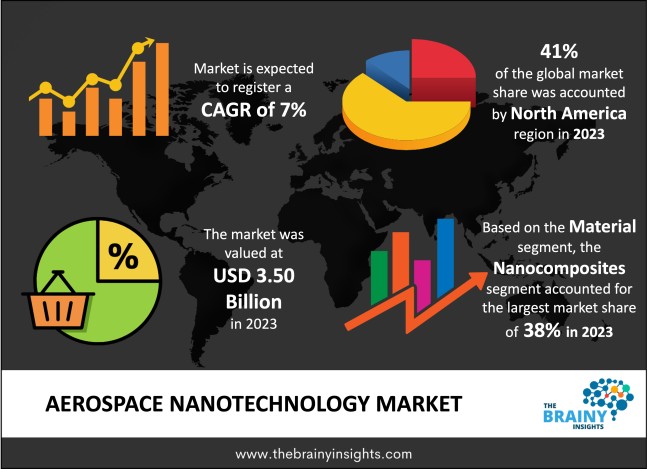

The global aerospace nanotechnology market was valued at USD 3.50 billion in 2023 and grew at a CAGR of 7% from 2024 to 2033. The market is expected to reach USD 6.88 billion by 2033. The increasing expenditure on avionics and the aerospace industry will drive the growth of the global aerospace nanotechnology market.

Aerospace nanotechnology can be defined as a technological sub-field that applies engineering and manufacturing for improvement of aerospace system attributed to the properties of materials at the nanoscale. On the nanoscale materials have different physical and chemical properties, which fundamentally differ from the properties of the material studied on a macroscale. Nanotechnology performs an updated function of material science in the aerospace industry including nanocomposites as well as nanostructure coatings. Furthermore, through nanotechnology, it is possible to design structures with several functions within one system owing to integrated functional components. These things include self-healing materials. Additionally, the value-added features of the nanoscale coatings will be useful in thermal shielding, corrosion, and drag control that can lead to enhanced efficiency in the aerospace systems. Incorporation of nanoscale materials into electronic circuits can lead to miniaturization and enhancing the essentials used in avionic and communication systems. Besides, the aerospace application of nanotechnology can also optimize power devices like batteries and fuel cells. These outcomes can improve the propulsion systems, and consequently help create the greener and more sustainable aerospace technologies.

Get an overview of this study by requesting a free sample

Increased investment in advancing the aerospace industry – governments and other private entities understand the revolutionary effect that nanomaterials could bring to aerospace industry and its various features such as performance, safety and sustainability. As a result, both federal and private sources are providing huge funding support directed towards advancement and commercialization of nanotechnology. Rewards and grants are also amongst the governmental strategies that augment the advancement of aerospace industry. These kinds of investments do not only advance research but also consolidate partnerships between universities and research bodies and the industry players. Similarly, aviation manufactures are gradually investing in heavy amounts of technological research and development. The competition in aerospace industry also forces organizations to maintain competitiveness with the help of nanotechnology that may add value into products and services offered to customers by meeting greater demands for efficiency and sustainability.

High development and manufacturing costs – The fixed capital costs include high initial expenditure for research and development (R&D). These are usually expensive due to the nature of commodities, costly equipment, appropriate facilities, and expert human resource. Inventing novel nanomaterials means demanding experiments, which may be rather a lengthy process and require many resources. This involves not only the manufacturing of nanomaterials but also strenuous evaluation of its effectiveness, toxicity, and compatibility with the aerospace systems. Chemical vapor deposition, sol-gel processes and electrospinning are some of the techniques used in production of nanomaterials which might be a challenge to acquire in all the aerospace firms. Such methods are characteristically expensive to implement given the cost of the reagents, time, energy, and most require aseptic conditions thus requiring elaborate and costly sterility. Therefore, the high development and manufacturing costs will hamper the market’s growth.

Technological advancements – Advancements in methods of nanofabrication, like Chemical Vapor Deposition, sol gel synthesis, and electrospinning have enhanced production of nanomaterials. Furthermore, new development in characterization technologies including Atomic Force Microscopy (AFM) and Scanning Electron Microscopy (SEM) have advanced researchers on the characterization and understanding of nanomaterials at molecular level. Additionally, the advanced manufacturing technique such as 3D printing has completely changed the model of fabrication of aerospace parts. This does not only improve the design freedom but also minimize wastage of resources in manufacturing. Integration of AI and machine learning is improving the design of materials and enhancing performance, facilitating a quick prototyping and testing of nanomaterials for aerospace uses. Therefore, these evolving technologies are leading the development of the aerospace nanotechnology and contributing to the market’s growth.

The regions analyzed for the market include North America, Europe, South America, Asia Pacific, the Middle East, and Africa. North America emerged as the most significant global aerospace nanotechnology market, with a 41% market revenue share in 2023.

Many large aerospace manufacturers are located in this area such as Boeing, Lockheed Martin, and Northrop Grumman that are most actively pushing nanotechnology into space. Similarly, the availability of prominent research institutes and universities add on to the fact that North America region leads this particular technology. Further, North American region has a robust legal provision in aerospace, and it guarantees the quality of materials and technologies. This focus on strict safety measures put pressure on the manufacturers to search for new technologies and thus increase the application of nanotechnology. With the current increase in space exploration activities across the world, North America dearly stands out as a region that is keen on developing the future complex aerospace systems with nanotechnology to improve the capabilities.

North America Region Aerospace Nanotechnology Market Share in 2023 - 41%

www.thebrainyinsights.com

Check the geographical analysis of this market by requesting a free sample

The material segment is divided into nanocomposites, nanostructured coatings, nanotubes and nanofibers, and nanoscale additives. The nanocomposites segment dominated the market, with a market share of around 38% in 2023. Nanocomposites is the largest material category in aerospace nanotechnology market because they offer remarkable improvements in properties over base materials. These advanced composites materials are produced through reinforcing polymers, metals or ceramics at the nanoscale level using carbon nanotubes, Graphene, or Nano-silica. The most important benefit of nanocomposites is its ability to be lightweight, which is especially desirable in the aerospace industry as lighter planes and space vehicles translates in fuel conservation and improved performance. This characteristic is important to meet growing regulatory demands to address sustainability and emission challenges and operate with a lower cost base for serving the commercial aviation market. The tunability of the properties of nanocomposites also make them suitable for diverse specific use depending on the requirements of that segment of the aerospace industry. Furthermore, the advancement research and development in nanocomposite technologies are to expected to expound its dominance in aerospace nanotechnology market.

The application segment is divided into aerospace structures, propulsion systems, avionics and electronics, and fuel systems. The aerospace structures segment dominated the market, with a market share of around 36% in 2023. The aerospace structures remain the largest application segment of the aerospace nanotechnology market mainly because the aerospace structures need lightweight, high strength, and durable materials in aerospace engineering. Since fuel efficiency depends on structure performance to a large extent, the aerospace industry is primarily geared at optimizing structural design for high performance and reduced weight, essential for cost savings. Nanomaterials within carbon nanotubes or graphene incorporating into the conventional substrates known as nanocomposites offer excellent strength-to-weight ratios allow aerospace industries to develop frame and other structural elements, which are comparatively lightweight and much more resistant as compare to normal materials. This reduction in weight also leads to increase in payload or the environmentally friendly engine that makes the aircraft cheaper to operate. Besides, the nanoscale coatings may improve wear and corrosion protection, thermal stability, and damage tolerance in aerospace structures and their further service life and reliability.

The end user segment is divided into commercial aviation, military aviation, space exploration, and unmanned aerial vehicles (UAVs). The space exploration segment dominated the market, with a market share of around 42% in 2023. Extreme environmental factors such as temperature variations, harsh and vacuum environment, radiation among others calls for high end technologies and materials that are resistant to the above environmental factors and most importantly offer safety to human resource in space. Nano technology offers solutions that meet these needs specifically. There is growing use of nanocomposites in space vehicle structures, which can provide necessary strength to weight ratios and thermal stability, which are important for launch vehicle and satellite applications. One of the advantages of such materials is their relatively low weight, which in turn enables the reduction of the costs of the missions, and therefore increase the feasibility of the missions. Finally, nanoscale coatings of TPS can improve the reliability and service life of the spacecraft. In addition, nanotechnology plays a role in enhancing complex electronics and sensor applications for space missions. Nanoscale materials have the potential to create small and efficient electronics and contribute to the development of more compact means for recording information and sending it from one point to another. This is particularly important for missions where high-performance instruments are to be accommodated within a restricted volume.

| Attribute | Description |

|---|---|

| Market Size | Revenue (USD Billion) |

| Market size value in 2023 | USD 3.50 Billion |

| Market size value in 2033 | USD 6.88 Billion |

| CAGR (2024 to 2033) | 7% |

| Historical data | 2020-2022 |

| Base Year | 2023 |

| Forecast | 2024-2033 |

| Region | The regions analyzed for the market are Asia Pacific, Europe, South America, North America, and Middle East and Africa. Furthermore, the regions are further analyzed at the country level. |

| Segments | Material, Application and End User |

As per The Brainy Insights, the size of the global aerospace nanotechnology market was valued at USD 3.50 billion in 2023 to USD 6.88 billion by 2033.

Global aerospace nanotechnology market is growing at a CAGR of 7% during the forecast period 2024-2033.

The market's growth will be influenced by increased investment in advancing the aerospace industry.

High development and manufacturing costs could hamper the market growth.

This study forecasts revenue at global, regional, and country levels from 2020 to 2033. The Brainy Insights has segmented the global aerospace nanotechnology market based on below mentioned segments:

Global Aerospace Nanotechnology Market by Material:

Global Aerospace Nanotechnology Market by Application:

Global Aerospace Nanotechnology Market by End User:

Global Aerospace Nanotechnology Market by Region:

Research has its special purpose to undertake marketing efficiently. In this competitive scenario, businesses need information across all industry verticals; the information about customer wants, market demand, competition, industry trends, distribution channels etc. This information needs to be updated regularly because businesses operate in a dynamic environment. Our organization, The Brainy Insights incorporates scientific and systematic research procedures in order to get proper market insights and industry analysis for overall business success. The analysis consists of studying the market from a miniscule level wherein we implement statistical tools which helps us in examining the data with accuracy and precision.

Our research reports feature both; quantitative and qualitative aspects for any market. Qualitative information for any market research process are fundamental because they reveal the customer needs and wants, usage and consumption for any product/service related to a specific industry. This in turn aids the marketers/investors in knowing certain perceptions of the customers. Qualitative research can enlighten about the different product concepts and designs along with unique service offering that in turn, helps define marketing problems and generate opportunities. On the other hand, quantitative research engages with the data collection process through interviews, e-mail interactions, surveys and pilot studies. Quantitative aspects for the market research are useful to validate the hypotheses generated during qualitative research method, explore empirical patterns in the data with the help of statistical tools, and finally make the market estimations.

The Brainy Insights offers comprehensive research and analysis, based on a wide assortment of factual insights gained through interviews with CXOs and global experts and secondary data from reliable sources. Our analysts and industry specialist assume vital roles in building up statistical tools and analysis models, which are used to analyse the data and arrive at accurate insights with exceedingly informative research discoveries. The data provided by our organization have proven precious to a diverse range of companies, facilitating them to address issues such as determining which products/services are the most appealing, whether or not customers use the product in the manner anticipated, the purchasing intentions of the market and many others.

Our research methodology encompasses an idyllic combination of primary and secondary initiatives. Key phases involved in this process are listed below:

The phase involves the gathering and collecting of market data and its related information with the help of different sources & research procedures.

The data procurement stage involves in data gathering and collecting through various data sources.

This stage involves in extensive research. These data sources includes:

Purchased Database: Purchased databases play a crucial role in estimating the market sizes irrespective of the domain. Our purchased database includes:

Primary Research: The Brainy Insights interacts with leading companies and experts of the concerned domain to develop the analyst team’s market understanding and expertise. It improves and substantiates every single data presented in the market reports. Primary research mainly involves in telephonic interviews, E-mail interactions and face-to-face interviews with the raw material providers, manufacturers/producers, distributors, & independent consultants. The interviews that we conduct provides valuable data on market size and industry growth trends prevailing in the market. Our organization also conducts surveys with the various industry experts in order to gain overall insights of the industry/market. For instance, in healthcare industry we conduct surveys with the pharmacists, doctors, surgeons and nurses in order to gain insights and key information of a medical product/device/equipment which the customers are going to usage. Surveys are conducted in the form of questionnaire designed by our own analyst team. Surveys plays an important role in primary research because surveys helps us to identify the key target audiences of the market. Additionally, surveys helps to identify the key target audience engaged with the market. Our survey team conducts the survey by targeting the key audience, thus gaining insights from them. Based on the perspectives of the customers, this information is utilized to formulate market strategies. Moreover, market surveys helps us to understand the current competitive situation of the industry. To be precise, our survey process typically involve with the 360 analysis of the market. This analytical process begins by identifying the prospective customers for a product or service related to the market/industry to obtain data on how a product/service could fit into customers’ lives.

Secondary Research: The secondary data sources includes information published by the on-profit organizations such as World bank, WHO, company fillings, investor presentations, annual reports, national government documents, statistical databases, blogs, articles, white papers and others. From the annual report, we analyse a company’s revenue to understand the key segment and market share of that organization in a particular region. We analyse the company websites and adopt the product mapping technique which is important for deriving the segment revenue. In the product mapping method, we select and categorize the products offered by the companies catering to domain specific market, deduce the product revenue for each of the companies so as to get overall estimation of the market size. We also source data and analyses trends based on information received from supply side and demand side intermediaries in the value chain. The supply side denotes the data gathered from supplier, distributor, wholesaler and the demand side illustrates the data gathered from the end customers for respective market domain.

The supply side for a domain specific market is analysed by:

The demand side for the market is estimated through:

In-house Library: Apart from these third-party sources, we have our in-house library of qualitative and quantitative information. Our in-house database includes market data for various industry and domains. These data are updated on regular basis as per the changing market scenario. Our library includes, historic databases, internal audit reports and archives.

Sometimes there are instances where there is no metadata or raw data available for any domain specific market. For those cases, we use our expertise to forecast and estimate the market size in order to generate comprehensive data sets. Our analyst team adopt a robust research technique in order to produce the estimates:

Data Synthesis: This stage involves the analysis & mapping of all the information obtained from the previous step. It also involves in scrutinizing the data for any discrepancy observed while data gathering related to the market. The data is collected with consideration to the heterogeneity of sources. Robust scientific techniques are in place for synthesizing disparate data sets and provide the essential contextual information that can orient market strategies. The Brainy Insights has extensive experience in data synthesis where the data passes through various stages:

Market Deduction & Formulation: The final stage comprises of assigning data points at appropriate market spaces so as to deduce feasible conclusions. Analyst perspective & subject matter expert based holistic form of market sizing coupled with industry analysis also plays a crucial role in this stage.

This stage involves in finalization of the market size and numbers that we have collected from data integration step. With data interpolation, it is made sure that there is no gap in the market data. Successful trend analysis is done by our analysts using extrapolation techniques, which provide the best possible forecasts for the market.

Data Validation & Market Feedback: Validation is the most important step in the process. Validation & re-validation via an intricately designed process helps us finalize data-points to be used for final calculations.

The Brainy Insights interacts with leading companies and experts of the concerned domain to develop the analyst team’s market understanding and expertise. It improves and substantiates every single data presented in the market reports. The data validation interview and discussion panels are typically composed of the most experienced industry members. The participants include, however, are not limited to:

Moreover, we always validate our data and findings through primary respondents from all the major regions we are working on.

Free Customization

Fortune 500 Clients

Free Yearly Update On Purchase Of Multi/Corporate License

Companies Served Till Date